Here's a statement of the obvious: The opinions expressed here are those of the participants, not those of the Mutual Fund Observer. We cannot vouch for the accuracy or appropriateness of any of it, though we do encourage civility and good humor.

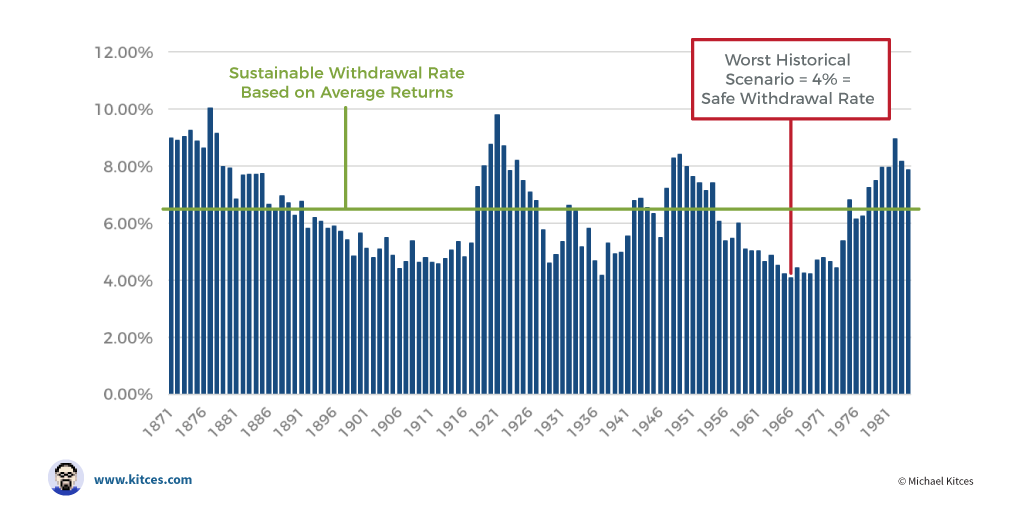

Kitces or Bengen, what I like about the research is the reminder that 1929 was not the worst case--the mid-1960s were the worst case. That's because the test portfolio is a balanced mix of stocks and bonds, and withdrawal dollars are adjusted for inflation each year.

After 1929, the bonds in the mix cushioned the decline, and the 25% deflation in the early 1930s allowed dollar withdrawals to be reduced, easing the burden on the shrunken portfolio.

But in the 1960s, bonds went down with stocks, and inflation roared, causing dollar withdrawals to increase dramatically against the jointly declining portfolio.

"His original paper was based on just two asset classes, intermediate-term Treasury bonds and large-cap stocks. He has since concluded that by adding a third asset class, small-cap stocks, investors could safely withdraw as much as 4.5% annually."

If of interest, the Trinity study is another in this vein (they used a broader mix of asset classes, but also found the 1960s to be the most perilous point). The wikipedia article links to some follow on research: https://en.wikipedia.org/wiki/Trinity_study

"His original paper was based on just two asset classes, intermediate-term Treasury bonds and large-cap stocks. He has since concluded that by adding a third asset class, small-cap stocks, investors could safely withdraw as much as 4.5% annually."

In building the OP, I captured the link to the "image" and also to the more detailed referenced "article" that I thought would be more useful. I didn't provide the link to tweet itself (above). But I see now that the article and chart are from 5 years ago. I also see that you have posted a comment on that article's feed (below) TODAY and let us see if there is a response, https://www.kitces.com/blog/safe-withdrawal-rate-calculator-software-big-picture-timeline-app-reviews/#comment-5935337942

May be you can engage him on Twitter if you are there.

Probably because the first six months of 2022 caused a lot of panic among the SWR crowd, with stocks and bonds falling sharply together, thus threatening the idea that a balanced fund will sail you through any storm. I interpret the Kitces tweet as in the vein of "stay the course." Even Bengen was wavering, in that piece I cited above.

Comments

Kitces or Bengen, what I like about the research is the reminder that 1929 was not the worst case--the mid-1960s were the worst case. That's because the test portfolio is a balanced mix of stocks and bonds, and withdrawal dollars are adjusted for inflation each year.

After 1929, the bonds in the mix cushioned the decline, and the 25% deflation in the early 1930s allowed dollar withdrawals to be reduced, easing the burden on the shrunken portfolio.

But in the 1960s, bonds went down with stocks, and inflation roared, causing dollar withdrawals to increase dramatically against the jointly declining portfolio.

First six months of 2022 anyone?

(Jan of last year.)

from

https://www.barrons.com/articles/the-originator-of-the-4-retirement-rule-thinks-its-off-the-mark-he-says-it-now-could-be-up-to-4-5-51611410402

If of interest, the Trinity study is another in this vein (they used a broader mix of asset classes, but also found the 1960s to be the most perilous point). The wikipedia article links to some follow on research: https://en.wikipedia.org/wiki/Trinity_study

can't quite figure out why he referred to it recently

https://twitter.com/MichaelKitces/status/1553821828153577475

In building the OP, I captured the link to the "image" and also to the more detailed referenced "article" that I thought would be more useful. I didn't provide the link to tweet itself (above). But I see now that the article and chart are from 5 years ago. I also see that you have posted a comment on that article's feed (below) TODAY and let us see if there is a response,

https://www.kitces.com/blog/safe-withdrawal-rate-calculator-software-big-picture-timeline-app-reviews/#comment-5935337942

May be you can engage him on Twitter if you are there.

It appears i-ORP retirement is offline. Have you found a work around to this retirement software planner? I really like the features of this planner.

Related Article on the Planner:

https://mydollarplan.com/optimal-retirement-planner/

i-ORP link (is off line):

i-orp.com/

the-hidden-peril-in-sequence-of-returns-risk