It looks like you're new here. If you want to get involved, click one of these buttons!

As part of his remarks offering some broader advice about investing at his company’s first-ever virtual annual meeting on May 2 [2020], Buffett said, “In my view, for most people, the best thing to do is to own the S&P 500 index fund,” which would track the S&P 500.

Yes, used to own it and it sits just below VWIAX and FMSDX on my 30%-50% list. Its 2020 blowout year jumped it to the top TR performer of the three. It is however largely a LC/MC Growth fund on the stock side. I prefer to get that exposure through the higher stock allocation AA funds and dedicated Growth funds. That said, if I added another 30%-50% AA fund, this would likely be it.Stillers, have you had occasion to look at the variants of AIGPX (available at Wells with low minimum)?

I've got some PONAX but expenses keep rising and the fund seems to be struggling since the management changes. I have LBNDX on my radard to replace my PONAX. That said, both LBNDX anda GIBLX (better longer term) have really high turnover rates.Year-end portfolio tinkering.

Me thinks perhaps the market forces the Fed unleashed in March 2020 will continue to play out in 2021 as vaccines get distributed. With that in mind, a couple of "exotic" funds were added to the fund portfolio.

Bond Pot: Added SVARX. Sold PFOAX. Pot includes PTIAX, PONAX, RCTIX, SVARX, IOFIX. IOFIX will probably be eliminated as it continues to recover in 2021 (replace with GIBLX or ?).

Mixed I Pot: Added GBLMX. Sold HBLAX. Pot includes VWINX, GBLMX, DHHIX, PFANX, TRECX.

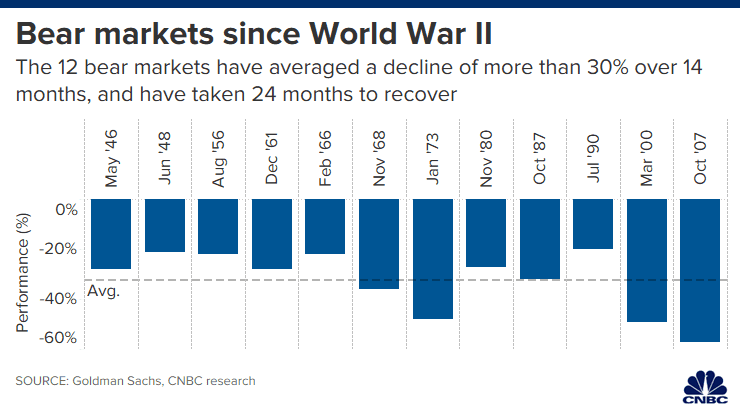

I did not panic, I trust, and was not trying to time, in the usual sense. By May 11 all of our equity fund holdings were back to breakeven or abovewater (except for FRIFX, not a huge portion). I projected that this plague was going to be much worse and longer-lived than most were saying, which has turned out to be the case. (I'd lost to covid at end March my oldest college friend, of 55y nonstop acquaintance, healthy etc. --- a jarring, sudden-enough death.) I believed the economic impact was going to be much worse than predicted, including crippled consumer spending. Turned out to be only partly the case; certainly the latter did not occur. All this thinking of mine was informed by extensive reading and some crude numbercrunching. I thought if we could avoid a >20% monthslong / yearslong drop in this early stage of our retirement we would be better off. So as with so much in life I regret it only in hindsight.... can understand where you are coming from. If I panicked in March 2020, I would have missed out on a huge finish to 2020. I know we can't time the market ...

I'm not a professional, but I can understand your question. It seems to me that current (magnificent!) Market returns are due to the fact that stocks and bonds are utterly disconnected from "fundamentals." Governments everywhere have been busy "juicing" their economies due to the pandemic. Prior to the Covid thing, there was the "stimulus" to grease the gears again, following the Real Estate bubble and Crash back in 2008-09. I don't think all of that stimulus had ever been removed, since then. So, paraphrasing from something I read here a while ago: "The Markets are on a Methamphetamine bender." And when "ordinary," established big names do very well, they normally drag the small-caps and EM along with them. This is when those other sectors outperform.Ok... I somehow can't take my eyes off the drawdown on those sectors. So, given that, what is the takeaway? Because from various articles, energy and financials and small and mid caps along with emerging markets are supposed to be the 2021 winners. Is that because the drawdowns were so large in 2020? Still learning about drawdowns and why they are so important.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla