It looks like you're new here. If you want to get involved, click one of these buttons!

https://institutional.vanguard.com/investments/product-details/fund/4415Turnover rate excludes the value of portfolio securities received or delivered as a result of in-kind purchases or redemptions of the fund’s capital shares, including Vanguard ETF Creation Units.

Jeffrey M Colon, Unplugging Heartbeat Trades and Reforming the Taxation of ETFs, University of Chicago Business Law Review, Vol 2.1 (2022?), Section VII.Recognizing the potential benefits to ETFs and their shareholders of employing custom baskets, but also being cognizant of the potential for abuses, the SEC now permits virtually unfettered use of custom baskets. However, ETFs using these custom baskets must adopt and implement detailed written procedures that “set forth detailed parameters for the construction and acceptance of custom baskets that are in the best interest of the [ETF] and its shareholders . . . .” These written procedures are internal, non-public documents. Rule 6c-11 also permits ETFs to do heartbeat trades with non-APs on the day of a reorganization, merger, conversion, or liquidation.

https://www.bogleheads.org/forum/viewtopic.php?t=404611As an illustration of how well ETFs can avoid capital gains, Vanguard has had only three years in which its diversified stock ETFs distributed a gain.

Vanguard FTSE All-World Ex-US Small-Cap distributed small capital gains in 2009-2010, its first two years. It started near the 2009 market bottom and doubled in its first year, so it didn't have many stocks with losses to sell to meet index changes.

Vanguard International Dividend Achievers Index distributed a 6% capital gain in 2021, when it changed indexes and was thus forced to sell a lot of stock.

Among sector funds, Vanguard Consumer Staples ETF distributed a gain in 2004, its first year, and REIT Index has frequently distributed gains.

https://www.reddit.com/r/fidelityinvestments/comments/13y8iti/just_recently_noticed_that_on_dividend_pay_dates/For the Fidelity Plan, Fidelity will identify all owners of the security. Then, Fidelity Capital Market Services (FCMS) goes to the market for domestic securities to purchase securities for reinvestment two days before the payable date. Fidelity purchases as many shares as possible on a best-efforts basis, determines the average share prices, and then reallocates those shares proportionately to our clients. The reinvestment price is the average price of all shares purchased, which is determined by the market.

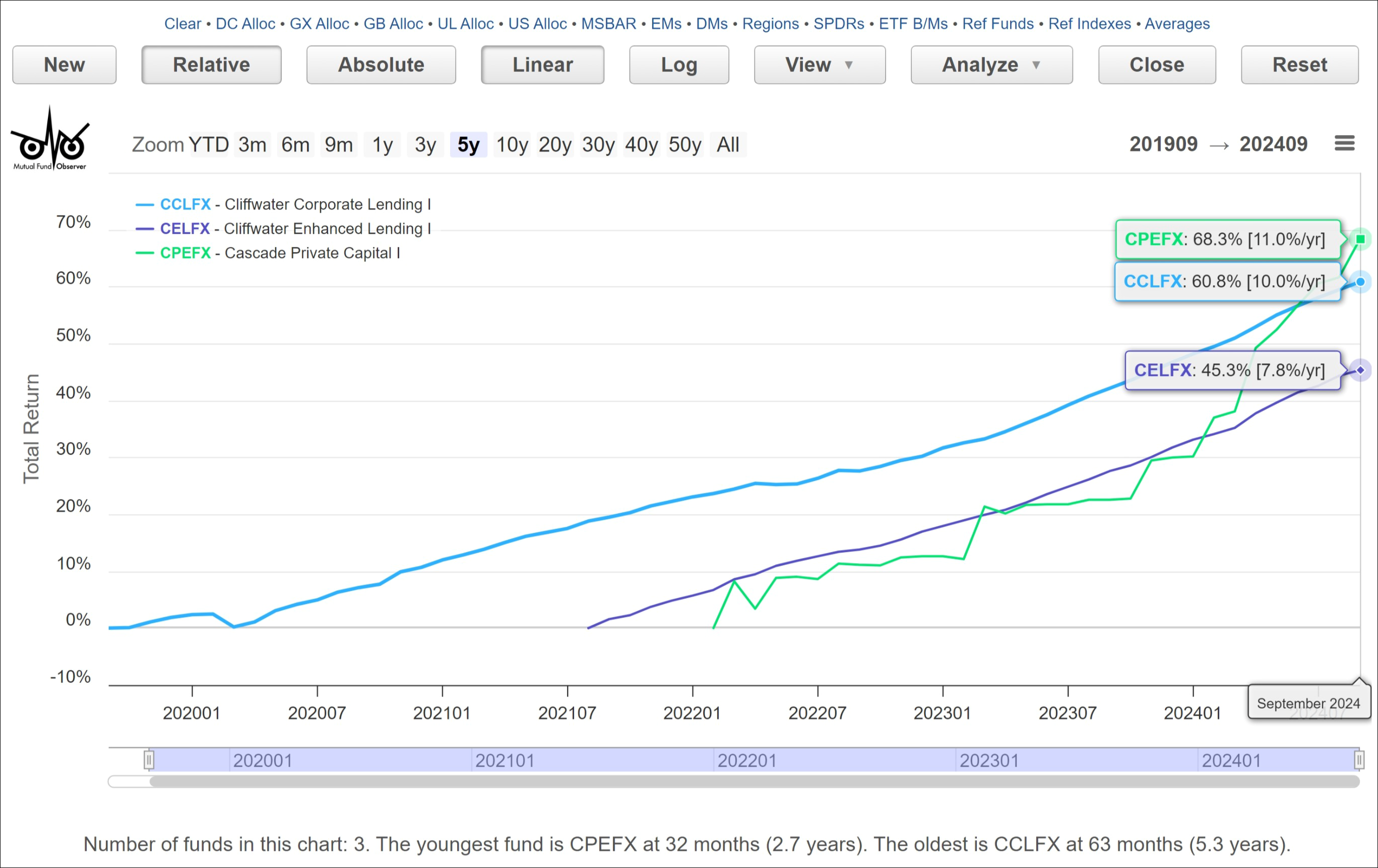

I sold THOPX earlier in the month as the volatility began eating into my gains. At around the same time I sold WSHNX and WCPNX. But they were nice funds when rates were dropping. Pretty much depends on where you think rates are heading from here.Is selecting THOPX performance chasing and I am going against my original criteria-low risk?

For the past two months, I have been following two "Market Neutral" funds, QQMNX and VMNFX, which held up very well and provided some protection during recent market downturns. New managers have been at the helm of both funds since 2021.

As MikeM said: "I have to admit, QQMNX is a tempting alternative in this alternative field for a less bumpy ride and, so far, excellent returns."

..............QQMNX....VMNFX

YTD.........15.6%.......8.9%

3 YRS.......14.4........14.8

5 YRS.......10.3..........8.2

2022..........9.5.........13.5

Std. Dev....8.6%.......7.3%

As a retired investor who doesn't need a lot more money, preserving capital is more important to me than seeking sizeable returns on capital. While both funds have excellent risk/reward profiles, I have decided to add QQMNX to my portfolio at this time of fairly high equity valuations.

A couple other market neutral funds you can consider: BDMAX and JMNAX. BDMAX has outperformed QQMNX over the last 1 and 2 year trailing periods, and has a higher Sharpe ratio and lower standard deviation over the last 3 years according to Morningstar data. JMNAX has had lower returns, but has a smooth ride. I use a combination of BDMAX and JMNAX, but I might consider adding QQMNX. Thanks for bringing it up.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla