IOFIX - I guess it works until it doesn't Alphacentric just released this letter. I'm not sure this relieves my concerns. It doesn't explain the steep drops:

March 20, 2020

Valued Investor,

We appreciate your commitment in the AlphaCentric Income Opportunities Fund IOFIX | IOFCX | IOFAX, especially

during periods of uncertainty and volatility. We believe the Fund is positioned well for this low mortgage rate

environment.

Markets have seen an enormous amount of cash being raised out of fear over COVID-19.

The recent NAV decline in our Fund is largely technically driven. On the flip side, the large draw down in the

corporate world, in both equities and bonds, can mostly be explained through deteriorating fundamentals (ex.

massive drop in airline, hotel, restaurant, retail, travel revenues).

While we are prepared for potential continued technical volatility, longer-term we are as confident as ever in the

fundamentals of our portfolio and believe the current rate environment may accelerate upside returns for our

Fund.

Here are the underlying reasons:

• Legacy mortgages originated back in 2002-2007, are 13-18 years old, why this is important:

o These borrowers made it through the worst housing crisis ever in 2008/2009.

o They have on average 43% equity in their homes today and have spent over a decade building

this equity.

o A good portion of their monthly payment today is on principal.

• YTD mortgage rates have dropped around 17% to historical lows, why this is important:

o Lower rates = increase in refinancing by homeowners and bond calls by service providers.

o Many of the legacy bonds that we paid less than par for are now likely to be paid off at or near

par.

o The increase in refinancing and foreseeable bond calls sets the table for nice price appreciation

over the next 12-18 months, in addition to the monthly income.

o Average price of the homes in the portfolio is around $260k, this segment of the housing market

continues to remain strong with low rates and a shortage of homes.

• Unlike corporate debt, our bonds are backed by hard assets - homes with real equity and in many cases,

the biggest asset a homeowner has.

o 10 out of the last 11 recessions have had minimal impact on housing.

o The Government provided many mortgage assistance programs to keep homeowners in their

house during the last recession and now, more than ever, it is of the utmost importance for

homeowners to stay put in their homes and away from others.

o In many cases, homeowner's two largest expenses, mortgage and energy, just got reduced.

o The Fund has no exposure to CLO's, CMBS, consumer credit, etc...just housing.

This will not continue forever, and as always markets will eventually stabilize. We know that being an investor

today, and during any period isn't exactly a stress-free experience, but we believe value investors should consider

adding to this portfolio.

Please let me know if you have any questions. If you would like to schedule a call with one of the portfolio

managers, we are happy to schedule it.

Thank you,

AlphaCentric Advisors

Garrison Point Capital LLC

IOFIX - I guess it works until it doesn't IOFIX was only at a little over 2% of my portfolio when the storm hit, so its not a major hit for me. I feel for those who were more concentrated in it. I am a chicken little when it comes to concentrating my portfolio into any one "specialty" holding even if I have respect for the managers....which I did (and do) with IOFIX.

Thanks for that chart

@wxman123 . I, like many, am trying to figure out when to move in a substantial way to reenter the market of stocks. This history lesson from 1917 to 1918 is helpful in that regard. It suggests that at some point living with a pandemic becomes the new normal and gets priced into the market. So far I have been nibbling enough to keep the stock % in my portfolio from dropping significantly, but nothing more. I am currently inclined to wait at least until fall to see if there is a new surge in covid-19 cases then before moving back into stocks in a more substantial way.....assuming the initial surge peaks within the next several weeks. That will also provide time to get a sense for peoples willingness to restrict their interactions over an extended period of time as a vaccine is probably not going to be available any time soon.

IOFIX - I guess it works until it doesn't

Consider bond ladders for bear market peace of mind Https://www.dailycamera.com/2020/03/20/david-gardner-consider-bond-ladders-for-bear-market-peace-of-mind//David Gardner: Consider bond ladders for bear market peace of mind

By DAVID GARDNER |

To say the financial world has changed in the two weeks since my last column would be a vast understatement. A month ago we reached an all-time high in the S&P 500 large company index. There was a brief scare when it looked like China would not be able to control the outbreak of the novel coronavirus, but our stock market recovered after new cases started to recede. /

Anyone have experiences having 60/40 [but 40 have combined bond laddering portfolio]. Maybe all seasoned proof portfolio according to author

12 Bond Mutual Funds and ETFs to Buy for Protection You can't make this up. IOFAX and IOFIX are one of the funds featured in this article. It also includes MINT which I bailed out of earlier this week as it was minting capital losses daily !

Federal Reserve Gives Emergency Aid to Mutual Funds Good find. Here's the Fed's PR piece and the actual term sheet.

https://www.federalreserve.gov/newsevents/pressreleases/monetary20200320b.htmhttps://www.federalreserve.gov/newsevents/pressreleases/files/monetary20200320b1.pdfCNBC: "However, continued disruption in the markets for state and local government debt promoted the Fed to take further action in its efforts to combat coronavirus effects."

CNBC is saying that the reason for not having done this initially was door number 2 - that the government didn't think the muni market was sufficiently unstable. I'm not convinced, and think that doors one (poor communication) and three (reluctance to touch non-federal securities) are still possible explanations. Doesn't matter now, though.

A key difference between the way muni MMFs and everything else is being handled is that if a loan is made to anything else, the loan rate is set at

prime plus 1%. For the muni MMFs, it's just prime plus 0.25%.

Federal Reserve Gives Emergency Aid to Mutual Funds That's a good question. These days I haven't been paying too much attention to muni MMFs because they're paying less than online bank accounts (after tax). So it doesn't make much sense to take on their additional risk. (Aside from considerations like Medicare IRMAA where gross income is what matters.)

It's hard to read into the government announcement.

It could be that the wording was sloppy and the intent was to cover prime and muni MMFs. (I checked the

N-MFP filing for VMSXX to verify that it is not considered a prime fund.)

It could be that the government doesn't consider muni MMFs to be at enough risk to offer this loan option.

It could be that the government does consider muni MMFs to be at higher risk but doesn't want to handle non-federal securities as collateral for its loans.

FWIW, the true NAV of VMSXX over the past six months has been consistently over $1, ranging between $1.0001 and $1.0004 until the past three days where it dropped to $0.9998, $0.9995, and $0.9992 as of yesterday. Fidelity's FMOXX has generally had a higher NAV ($1.0012 to $1.0017), but it too has fallen in the last week from $1.0014 to $1.0007, likewise below its normal range.

Perhaps it is time to start watching these figures more closely.

msf,

Will this support VMSXX?

https://www.cnbc.com/2020/03/20/the-federal-reserve-is-expanding-its-asset-purchases-to-include-municipal-bonds.htmlMona

Would you buy a 50 year Treasury? Such ideas are being discussed in the Executive Branch.

White House economic adviser Larry Kudlow likes the idea, one of the people said. Treasury Secretary Steven Mnuchin, although initially skeptical, is now more willing to do it, the people said.

Do they really think they're going to get people to buy a fifty year bond for 2 - 3%? They've been having problems selling the tens.

How about 8%. I might think about buying such a thing at that yield.

But let's imagine 5% or 6%. All of a sudden that income annuity my wife can get from TIAA looks pretty good. So we sell out all the stocks and bonds in her IRA to finance it. And I start looking around for a reputable income annuity for my IRA. And I sell all the stuff in my IRA, if it's worth anything at that point.

There are probably rosier scenarios. Maybe someone could point one out to me.

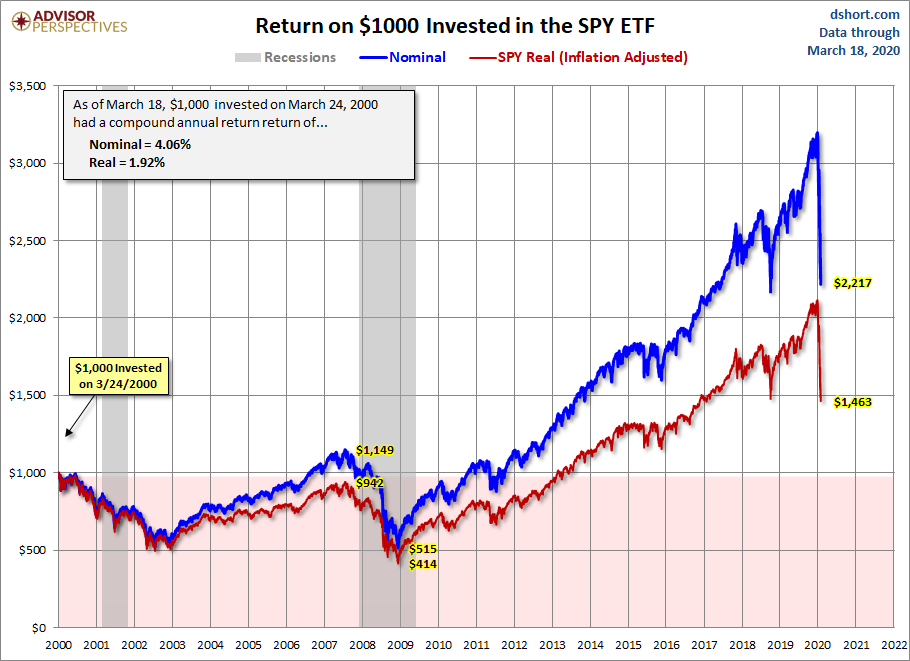

SPY and the 21st century. One ugly chart. This is not an example of technical analysis:

From DShort.com, AKA Advisor Perspectives -- as the graphic clearly states.

From DShort.com, AKA Advisor Perspectives -- as the graphic clearly states. .

I'm not sure this chart is anything more than an interesting look back in time. But if you have one of those friends who is always pestering you about buying the index . . . send him the link. But only if you have done better. ;-)

I used to follow the old dshort.com for his interesting charts through the thick of 2008 bust. Back in 2011 he sold to an outfit called Advisor Perspectives.

But

the charts continue to paint a picture of what is happening, courtesy of Jill Mislinski. And they publish a calendar of charts to come.

There is a variety of interesting articles and commentaries on the rest of the site if you poke around. You won't be assaulted by obvious advertising. But somebody is paying the bills. Here is their

about.

This recession is going to be bad. https://www.washingtonpost.com/opinions/2020/03/19/this-recession-is-going-be-bad-really-bad/?outputType=ampThis recession is going to be bad.

America has done something extraordinary, perhaps unprecedented. In the face of a looming public health crisis, with potential deaths in the thousands or even millions, we essentially made a collective decision to have ourselves a recession. We’ve shut down a significant portion of our economy, knowing that the result will be businesses going bankrupt, huge job losses and people losing their homes.

the single dumbest paragraph filed with the SEC this month I've been working on tracking down funds in the SEC pipeline (the Hypergrowth or Falling Knives ETFs, anybody?) and came across Terra Firma US Concentrated Realty Equity. Apparently it used to be some other fund, or funds, or portfolios. Despite naming the manager they won't name who he worked for when advising ... well, you'll see:

Performance data for the classes varies based on differences in their fee and expense structures. The performance figures for Open Class shares reflect the historical performance of the then-existing shares of the [...] (the “Predecessor Portfolio”) (the predecessor to the Fund, for which [...] served as the investment adviser), a series of [...], from September 23, 2011 to […], 2020. The performance figures for Open Class shares also reflect the historical performance of the then-existing shares of the predecessor fund to the Predecessor Portfolio, the [...] (the “Predecessor Fund”) (for which [...] served as the investment adviser), for periods prior to September 23, 2011. Jay P. Leupp has served as a portfolio manager for the Fund, the Predecessor Portfolio and the Predecessor Fund since December 31, 2008. Christopher J. Hartung has served as a portfolio manager for the Fund and the Predecessor Portfolio since 2018.

The aforementioned "Mr. Leupp was a Senior Portfolio Manager on [...]'s Global Real Estate Securities team from 2011 to 2019. Prior to joining [...] in 2011, Mr. Leupp was the President and Chief Executive Officer (“CEO”) of Grubb & Ellis Alesco Global Advisors."

(deep cleansing breath, deep cleaning breath, beer)

David

Why God made editorial TKTKs [to come]

The Rise of Green Bonds https://www.troweprice.com/financial-intermediary/is/en/thinking/articles/2020/q1/rise-green-bonds.html/the Rise of Green Bonds

Why investors should take a closer look at the green bond market.

Key Insights

Growth of the green bond market expected to continue in

2020, led by sovereigns.

Germany’s willingness to issue green bonds is likely to act as a reference point for other issuers.

There is an opportunity to start integrating green bonds into fixed income portfolios./

Trow price Dynamic Global Bond and Global Aggregate Bond

Anyone use these vehicles?

Energy -Oil jumps 13%, rebounding from Wednesday’s steep losses

Another buying opportunity @hank;you said," I don’t compute my returns daily or report them publicly.

End of this conversation, Derf

Not necessarily. If you send me a polite request (via the mfo mail service) sometime after December 31,

2020 I just might share my

2020 net gain / loss numbers with you. I do compute returns at the end of every year for my own purposes and store them in my data bank. However, what possible value to others such (unsubstantiated) data would provide is a bit of a mystery. Frankly, I think it’s silly to get excited about the last 2-3 months’ performance. Seasoned investors know that such data over short periods like that is pretty meaningless. It’s the aggregate compounded return over a number of years that matters.

In addition to being irrelevant and potentially misleading,

performance claims by

anonymous voices on an open forum like this are just that. Barring confirming specifics such as name, address, SS#, account numbers and certified statements from financial institutions these claims must be considered

unsubstantiated. That’s not an indictment of the forum. There’s a lot to be said for an informal and mostly anonymous arrangement like this.

You have caused me to rethink how I post. Some whom I respect mightily here have routinely declined to provide specifics regarding their investments / investment approach. But they’re great contributors in other ways. I suspect that in some cases they recognize that without providing personal and substantiating data, their claims would be of dubious value or open to suspicion. In other cases, I suspect it’s because they’re not certified to advise other investors and fear that by referencing their holdings they might inadvertently steer someone in the wrong direction.

In the future I’ll refrain in my board posts from mentioning any “buys” or “sells” or any mutual funds I own currently or have owned previously. Nor will I acknowledge any business associations I may have with any specific fund company or other fiduciaries or any associations I may have had in the past. Further, I’ll refrain from making any comment about perceived market valuation or direction. I won’t mention specific types of investments I own. And I won’t divulge my allocation to various assets. In essence, comments I’m not willing to substantiate by providing personal account-specific information have no place in this forum. Additionally, I’m not a certified financial advisor and so should not be opining about such matters as asset allocation, market valuations or direction.

Best regards

Coronavirus Selloff Leaves Just One U.S. Active Equity Mutual Fund Positive for the Year

the single dumbest paragraph filed with the SEC this month I've been working on tracking down funds in the SEC pipeline (the Hypergrowth or Falling Knives ETFs, anybody?) and came across Terra Firma US Concentrated Realty Equity. Apparently it used to be some other fund, or funds, or portfolios. Despite naming the manager they won't name who he worked for when advising ... well, you'll see:

Performance data for the classes varies based on differences in their fee and expense structures. The performance figures for Open Class shares reflect the historical performance of the then-existing shares of the [...] (the “Predecessor Portfolio”) (the predecessor to the Fund, for which [...] served as the investment adviser), a series of [...], from September 23, 2011 to […], 2020. The performance figures for Open Class shares also reflect the historical performance of the then-existing shares of the predecessor fund to the Predecessor Portfolio, the [...] (the “Predecessor Fund”) (for which [...] served as the investment adviser), for periods prior to September 23, 2011. Jay P. Leupp has served as a portfolio manager for the Fund, the Predecessor Portfolio and the Predecessor Fund since December 31, 2008. Christopher J. Hartung has served as a portfolio manager for the Fund and the Predecessor Portfolio since 2018.

The aforementioned "Mr. Leupp was a Senior Portfolio Manager on [...]'s Global Real Estate Securities team from 2011 to 2019. Prior to joining [...] in 2011, Mr. Leupp was the President and Chief Executive Officer (“CEO”) of Grubb & Ellis Alesco Global Advisors."

(deep cleansing breath, deep cleaning breath, beer)

David

Investor Bill Miller Calls This One of the Best Buying Opportunities of His Life coronavirus deaths < 200. Flu deaths between 22K to 55 = about 35-40,000. Corona is 10 times more deadly but we still have fewer deaths. Sure, we need to do all we do and be informed.

So far the SP500 fell about 30% from its top.

When to buy your first bucket? You got to use charts because it’s mechanical and many algos use it. I looked for several indicators that work for me and I used several but it’s too complicated. For Stocks: based on 2008 (which resembles

2020) the easiest is 100 moving average (Again, R48). 50+200 MA are the most used but 50 is too fast but 200 is too slow. MACD and looking at trends may confuse some/many. For CEF: use weekly MACD. For bond OEFs: use a simple chart trend. See below

Stocks: SP500 (

chart) from 2008 to 2009. See the 3 moving averages below. 100 MA(red line) is the best, not too early and not too late. For the current chart, you this (

link)

CEFs: PCI(

chart). Use weekly MACD and enter when it's positive

Bond OEFs: PIMIX (

chart). You want to see several weeks of uptrend

The stock market may bottom long before the coronavirus epidemic peaks, analysts say

Estimated Tax Computation Thanks for your reply, but what is your "sense" of what to expect in the way of dividends and capital gains distributions for 2020?