It looks like you're new here. If you want to get involved, click one of these buttons!

Earlier this month, David provided an update on the G/A conversion, which he originally discussed in his June 2020 MFO article.Don’t expect DFAU [US Core Equity] and DFAI [International Core Equity] to be the only DFA ETFs for very long, however. The firm just filed with the SEC to convert six of its tax-managed mutual funds into ETFs. That has never been done before, but at least one other firm, Guinness Atkinson, is attempting a similar conversion with one of its mutual funds.

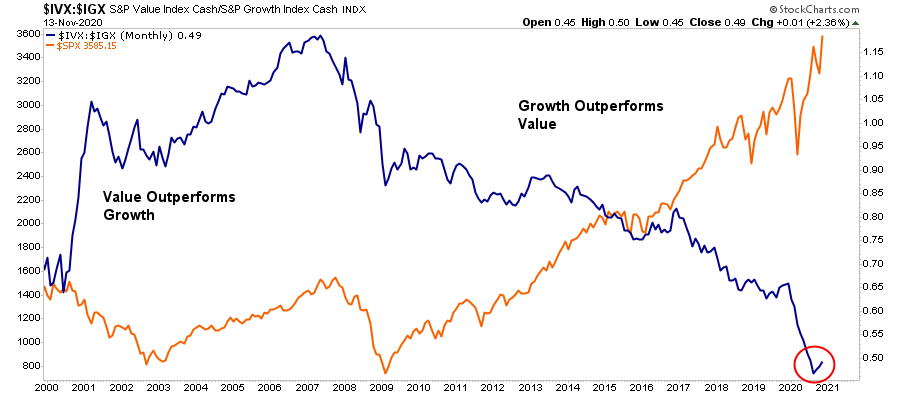

https://seekingalpha.com/article/4389100-market-breaks-out-on-vaccine-hopes-cases-surgeNotably, the rotation to "value" is likely premature as these companies specifically require a more robust economy to generate revenue and earnings growth. The current environment is not conducive to that. Expect a reversal of the trade soon, and money rotates back towards "pandemic" related companies.

I personally agree that taxes matter. I presently try to manage my taxable withdrawal verses tax free withdrawals to stay below (or at) the 12% tax bracket. Roth withdrawals have the advantage of being a tax free withdrawal.Roth money is often mentioned as the last pool of money that one should draw from.

If you often spend more money in your early days of retirement, would you not want to draw on Roth vs traditional to not realize the income for tax purposes?

JASVX - Hindsight is a great thing when you can look back until today :-)@FD1000Were they really big losses?I'm not a long term holder but a trader and avoided the big losses of March 2020.

If you had instead, not sold and just held your positions the draw down for JASVX was 6% in March of 2020. By May of 2020 you would have recovered from that loss without timing the market.

Had you been taking monthly withdrawals, those withdrawals would have been impacted slightly over 2 months. Having a 3-6 month cash position for withdrawals would solve that problem.

To be fair, IOFIX and SEMMX have yet to recover. Owning these two funds (that exhibit deep draw downs and slow recovers) may not the best choice for those seeking "yield with safety". I learn this the hard way owning THOPX.

cws-market-review-november-9-2020The ten worst-performing stocks this year through November 8 were up an average of 23% on Monday and Tuesday!

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla