Here's a statement of the obvious: The opinions expressed here are those of the participants, not those of the Mutual Fund Observer. We cannot vouch for the accuracy or appropriateness of any of it, though we do encourage civility and good humor.

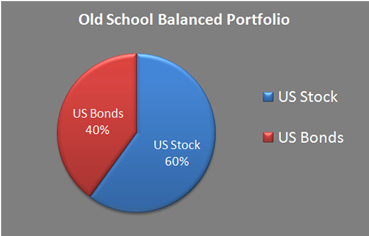

From Link: "Unlike a traditional two-asset 60/40 balanced fund, the 7Twelve balanced strategy utilizes multiple asset classes to enhance performance and reduce risk.

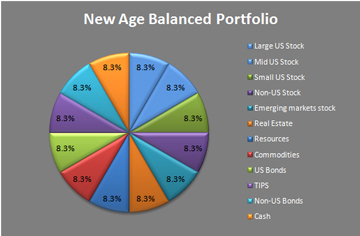

The 7 of 7Twelve represents the suggested number of asset classes to include in your portfolio. The Twelve represents the 12 separate mutual funds or exchange traded products to fully represent the 7 asset classes in your 7Twelve portfolio. Our portfolio has approximately a 65/35 allocation: approximately 65% of the portfolio is invested in equity and diversifying assets and about 35% invested in bonds and cash."

Do you have any other reference as to why this is a more sound way to balance a portfolio. All I saw in that article is how a set of allocations performed in the past against others. Forgive me, but one can simply tweak the asset allocations and come up with their own 6Fifteen portfolio, which is precisely what I think ,any of us do in our so called diversified portfolios.

So the very least it would be helpful if article offered some other measures, even though it would simply be historical data, such as sharpe ratio, Martin ratio, max dd, etc. otherwise I already "know" my entire portfolio should not consist of VBINX. I am not familiar with Isralesen, so appreciate if you can share some reference point of credibility.

I never understand the kind of allocation advocated, where every piece of the pie gets equal treatment. And the 25% in 'alternatives' could be problematic. Then there is the 8.3% in cash. Is this for planned withdrawals? If not, perhaps a ultra-short bond fund would be a more prudent option. Perhaps it would be better just to invest in a mix of 5-6 'dynamic allocation funds' like FPACX, TIBIX, MALOX, PRWCX, OAKBX, etc. In the end, there is no perfect allocation. The ideal allocation is one that an investor can live with when times are bad. I am not sure about this one.

Then there is the 8.3% in cash. Is this for planned withdrawals? If not, perhaps a ultra-short bond fund would be a more prudent option. Perhaps it would be better just to invest in a mix of 5-6 'dynamic allocation funds' like FPACX, TIBIX, MALOX, PRWCX, OAKBX, etc. In the end, there is no perfect allocation. The ideal allocation is one that an investor can live with when times are bad. I am not sure about this one.

I personally have no problem substituting "cash" with short term bonds or similar vehicles.

In another article by Israelsen as weighting in the other eleven pieces of the pie ebb and flow the cash position is available to help rebalance those positions.

There also is an age based adjustment to cash with his allocation strategies. From 50-60 years of age his startegy raises cash (from 8.3% to 20% cash), 60-70 (40% cash), and 70+ (60% cash). I start to worry about "growing" a portfolio when holding this much cash. Cash can buoy a portfolio during market down drafts, but act too much like an anchor when markets rise.

Finally, judging by the performance of the the three cash/equity allocations compared to the two "non-cash indexes" he used as benchmarks (Vanguard's Balanced Index and Vanguard's S&P 500 Index), cash does seems to have a dampening effect of portfolio DD% as shown here (check out the yellow highlighted results for 2008):

@bee. It is not about him being a quack. It is about us swallowing what he is doling. I still don't see ANYTHING about his 7Twelve portfolio. If he is simply going to use past performance of some allocation and use percentage returns, then his having a PhD, and me not having one with my 6Fifteen portfolio gives Israelsen no credibility. Furthermore I'm not misspelling my last name

FWIW ... He was the first person that I came across (on web) that simply demonstrated the idea that one could construct a portfolio with more-or-less any exposure you want by combining a series of equal-weighted positions, that could then be grouped into various asset classes.

After I adopted this approach, it made the periodic rebalancing decision very easy - which position is now too high or low?

He also showed how you could use the "equal weighted positions" to effectively overweight (for example) small cap stocks.

Several years ago I explored the seven-twelve method by constructing a big spreadsheet comparing an investment of $1M in a balanced fund (VBINX) vs. the same $1M invested in various mutual funds (mostly index funds when I could find them) according to the 8 percent slices recommended for each (US midcap, global real estate, natural resources, and so on), over the 1988-2009 timeframe. It was a fun exercise. My conclusion was that for the majority of investors (not investing enthusiasts like us) its best to use a good low-cost balanced fund and be patient. The returns and volatility were essentially the same, and it was vastly simpler. If you'd like to see the spreadsheet, send me an email. I'm randynevin AT comcast DOT net.

Fascinating. And it's been beaten since say 9/08, 6y ago, beginning of the horrors and the reason one goes into good balanced funds to begin with, by MAPOX, ICMBX (great fund), and JABAX (another one, underknown bigtime).

Comments

Regards,

Ted

http://www.financial-planning.com/thought_leaders/israelsen.html

Do you have any other reference as to why this is a more sound way to balance a portfolio. All I saw in that article is how a set of allocations performed in the past against others. Forgive me, but one can simply tweak the asset allocations and come up with their own 6Fifteen portfolio, which is precisely what I think ,any of us do in our so called diversified portfolios.

So the very least it would be helpful if article offered some other measures, even though it would simply be historical data, such as sharpe ratio, Martin ratio, max dd, etc. otherwise I already "know" my entire portfolio should not consist of VBINX. I am not familiar with Isralesen, so appreciate if you can share some reference point of credibility.

In another article by Israelsen as weighting in the other eleven pieces of the pie ebb and flow the cash position is available to help rebalance those positions.

There also is an age based adjustment to cash with his allocation strategies. From 50-60 years of age his startegy raises cash (from 8.3% to 20% cash), 60-70 (40% cash), and 70+ (60% cash). I start to worry about "growing" a portfolio when holding this much cash. Cash can buoy a portfolio during market down drafts, but act too much like an anchor when markets rise.

Finally, judging by the performance of the the three cash/equity allocations compared to the two "non-cash indexes" he used as benchmarks (Vanguard's Balanced Index and Vanguard's S&P 500 Index), cash does seems to have a dampening effect of portfolio DD% as shown here (check out the yellow highlighted results for 2008):

financial-planning.com/thought_leaders/israelsen.html

If youe're asking me, "Is he a quack?"

Well, he does have a PHD after his name (so he may like to Piles it Higher and Deeper).

You could assemble your own AOK/AOM/AOR/AOA blend of blends and add commodity/resource/realty seasonings to taste, for an even simpler life.

As for this particular guy, creds are not terribly inspiring, really, though there's nothing wrong with that

https://fhssfaculty.byu.edu/ItemViewer.aspx?URL=ci28/pci/VITA CLI as of Jan 2011-1.pdf

Probably campus pals with the Yackts.

FWIW ... He was the first person that I came across (on web) that simply demonstrated the idea that one could construct a portfolio with more-or-less any exposure you want by combining a series of equal-weighted positions, that could then be grouped into various asset classes.

After I adopted this approach, it made the periodic rebalancing decision very easy - which position is now too high or low?

He also showed how you could use the "equal weighted positions" to effectively overweight (for example) small cap stocks.

I'm a fan.

http://whitecoatinvestor.com/150-portfolios-better-than-yours/

Dave