It looks like you're new here. If you want to get involved, click one of these buttons!

https://annuity.org/retirement/retirement-statistics/Three-quarters of Americans agree the country is facing a retirement crisis, making research around the topic more relevant than ever. We dug into the data on every angle of retirement and compiled the most important statistics below. Read on to learn about what today’s retirees face, from financial challenges to lifestyle decisions and more.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla

Comments

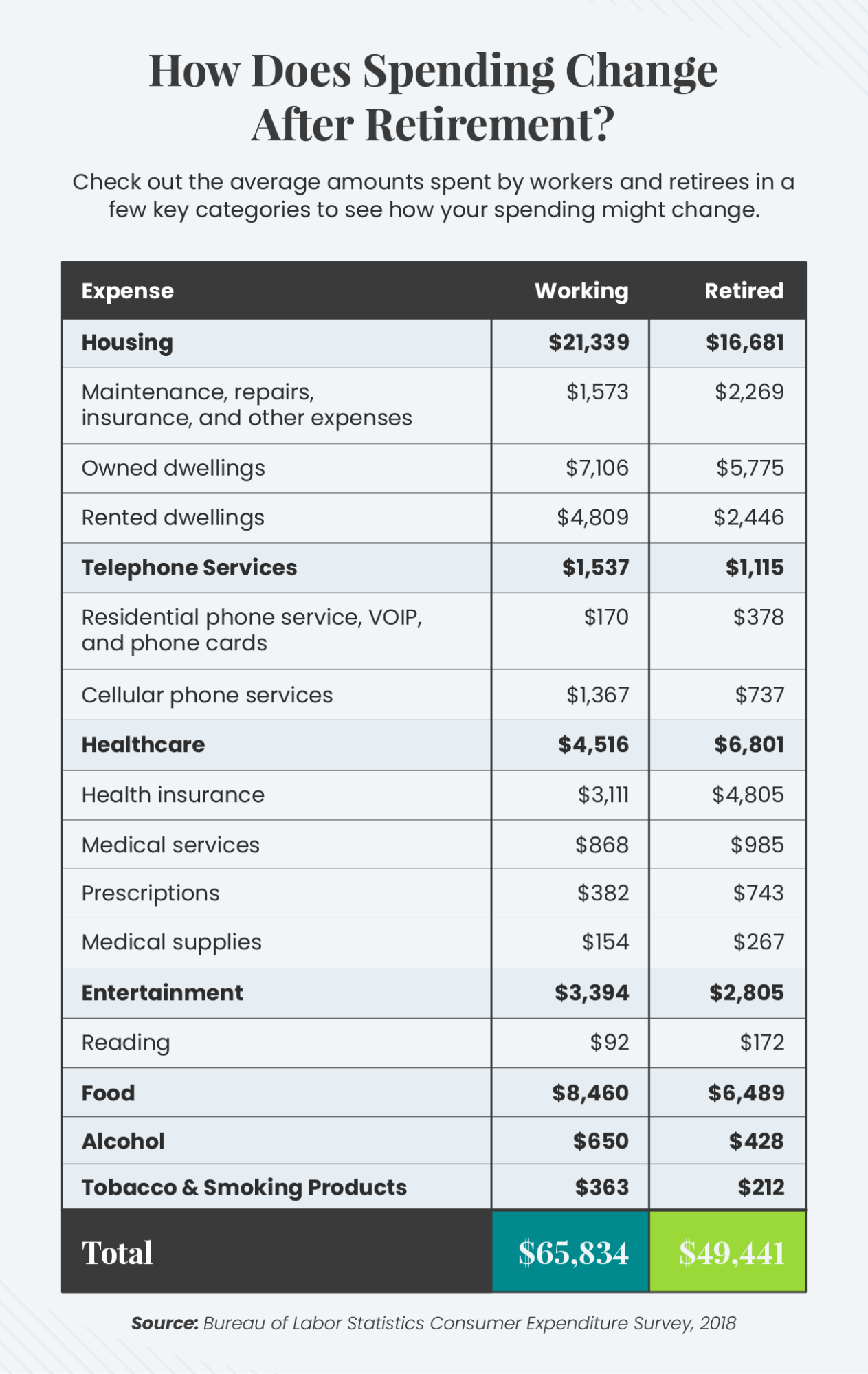

Noted NO funds for transportation .

Stay Kool, Derf

This dubious arithmetic extends to the bottom lines - they are much greater than the sum of the bolded components. I think that addresses @Derf 's observation that transportation isn't included. Apparently, transportation (including travel?) is not considered a "key category" (see text at top of chart).

Note that these are means, not medians. So while the text suggests that these figures illustrate how your spending might change in retirement, I'm not so sure.

Here's actual data from the 2018 BLS Consumer Expenditure Survey, by age. The numbers don't exactly match the table above, but they're close enough. The difference could be due to the fact that I'm looking at a column labeled "65 years and older", which is not the same as "retired".

https://www.bls.gov/cex/tables/calendar-year/mean-item-share-average-standard-error/reference-person-age-ranges-2018.pdf

FWIW, the mean transportation spending by a "consumer unit" with age 65+ is $7,270, while the national mean for consumer units is $9,761.

The BLS defines a "consumer unit" as: https://www.bls.gov/cex/csxgloss.htm#cu

Of course, since we're classifying by age, and a "consumer unit" consists of more than one person, we need to be clear on what "age" means for that unit. It's the age of the "reference person". https://www.bls.gov/cex/csxgloss.htm#refper

The article is from Annuity.org; so I'll place this in the advertising bin file.