It looks like you're new here. If you want to get involved, click one of these buttons!

https://abcnews.go.com/Business/soaring-gold-prices-warning-sign-economy/story?id=126414464The flight toward gold has coincided with a depreciation in the value of the U.S. dollar. Its value against other currencies plunged about 11% over the first half of 2025, the biggest decline in more than 50 years, a Morgan Stanley report in August found.

The decline in the U.S. dollar's value reflects a shift away from global dependence on the dollar as a global reserve currency, as investors take note of changes in U.S. economic policy and Trump's pressure campaign against the Fed, analysts said.

"Investors are getting nervous about all the traditionally safe U.S. assets like treasury securities," Pasquariello said. "Where else will they put money? Gold."

When prices are high and global conflicts destabilize the world, some investors start looking backwards—and what’s older and more dependable than gold?

Last week, amid widespread geopolitical turmoil and a weakening U.S. dollar, the price of gold hit a historic high of $4,000 an ounce. This year has so far been gold’s best since 1979, a moment of instability so profound that it led to recession.

Over the past 50 years, spikes in the price of gold have typically been correlated with widespread inflation and geopolitical dysfunction. The precious metal has long been considered a safe-haven asset, because, unlike the U.S. dollar, its inherent value isn’t determined by any state government.

Some investors see gold as a standard way to diversify their portfolio. Others, stereotypically known as goldbugs, tend to be broadly skeptical about contemporary monetary policy. Just as investors in bitcoin, so-called digital gold, have historically skewed libertarian and anti-institutional, the most extreme goldbugs are betting against the system, doubtful that the Federal Reserve is capable of keeping the U.S. dollar strong.

Gold prices have already risen more than 50 percent this year and are showing no signs of stopping. The story of today’s gold boom began in 2022, when Russia invaded Ukraine and Western governments decided to sanction the Russian central bank by freezing its foreign-exchange reserves. The scale of these sanctions was a reminder of why countries might want to own assets that can’t be easily frozen. Especially in emerging markets, central banks around the world “realized that the truly only safe asset” is gold.

The other main driver of this price spike is less abstract. Some Wall Streeters are concerned that the value of the U.S. dollar will continue to erode as the national debt climbs and the Federal Reserve loses its grip on the currency. They’re making what’s become known as the “Debasement Trade,” shifting money away from the weakening U.S. dollar and into harder, more independent assets such as gold and bitcoin. Shrinkflation, stagflation, good-old-fashioned inflation—all of it means that your paycheck doesn’t go as far as it once did, and all of it is good for gold.

The mystery of the current gold rally is that the S&P 500 is also up. The stock-market index reached an all-time high earlier this month, which would seem to suggest that the American economy isn’t quite as close to the brink as the price of gold might indicate.

But the reality probably has to do with a bifurcated market. Vanguard’s global chief economist told The New York Times on Saturday that this rare case of gold and stocks moving in a parallel upward trend has to do with “dramatically different” investor perspectives: The optimists are going with equities, and the pessimists are going with gold. In today’s economy, there’s room enough for both.

https://latimes.com/environment/story/2025-08-21/china-races-to-build-worlds-largest-solar-farm-to-meet-emissions-targetsChinese government officials last month showed off what they say will be the world’s largest solar farm when completed high on a Tibetan plateau. It will cover 235 square miles, which is the size of Chicago

Same Reuter's article as cited above.Under an environmental compliance strategy spearheaded by Greg Abel, chairman and chief executive of Berkshire Hathaway Energy, the company’s utilities have repeatedly and successfully resisted calls to install SCR scrubbers. That has saved billions of dollars, according to company disclosures, and afforded Berkshire plants lower operating costs.

https://www.reuters.com/investigations/buffetts-berkshire-hathaway-operates-dirtiest-set-coal-fired-power-plants-us-2025-01-14/Berkshire plants produce the most coal-fired electricity in the industry without the use of selective catalytic reduction systems, or SCR scrubbers, a technology that can reduce a coal plant’s NOx emissions by more than 80%. Available since the 1990s and more broadly adopted by Berkshire competitors, SCR scrubbers as of 2023 were employed at plants that generate 62% of the coal power in the U.S., EPA data show. At Berkshire, only 27% of its coal power was generated at coal-plant boilers with SCR scrubbers.

Putting AI to use.Cui bono?

I wonder who made the big bucks on the TACO trade between Friday and Monday? Who got the tip the Friday threat was coming? I've read that there were some profitable shorts in crypto on Friday.

https://cryptoslate.com/the-big-bitcoin-short-who-shorted-btc-before-trumps-tariff-post-to-bank-200-million/

Equity and ETF Markets

Trading data from major short-oriented exchange-traded funds (ETFs) show a clear increase in volume ahead of the announcement. The Direxion Daily FTSE China Bear 3X Shares (YANG) and ProShares UltraShort FTSE China 50 (FXP) — funds that profit when Chinese equities decline — experienced abnormally high trading volumes in the days leading up to October 10, when Trump first issued the tariff warning. The surge in those bearish funds coincided with a 6–7% plunge in U.S.-listed Chinese stocks immediately following the threats. This pattern suggests that some traders were positioning for downside risk before the news became public.

Crypto Markets and Insider Speculation

Separate reports indicate large short positions in Bitcoin and Ether placed roughly 30 minutes before Trump’s tariff announcement. The ensuing market crash wiped out almost $400 billion in crypto market value, while the anonymous investor allegedly made up to $200 million within 30 minutes. Analysts from CoinDesk said the timing and magnitude of those short positions “raise suspicion of information asymmetry,” fueling speculation that some traders may have had advance knowledge of the White House’s move.

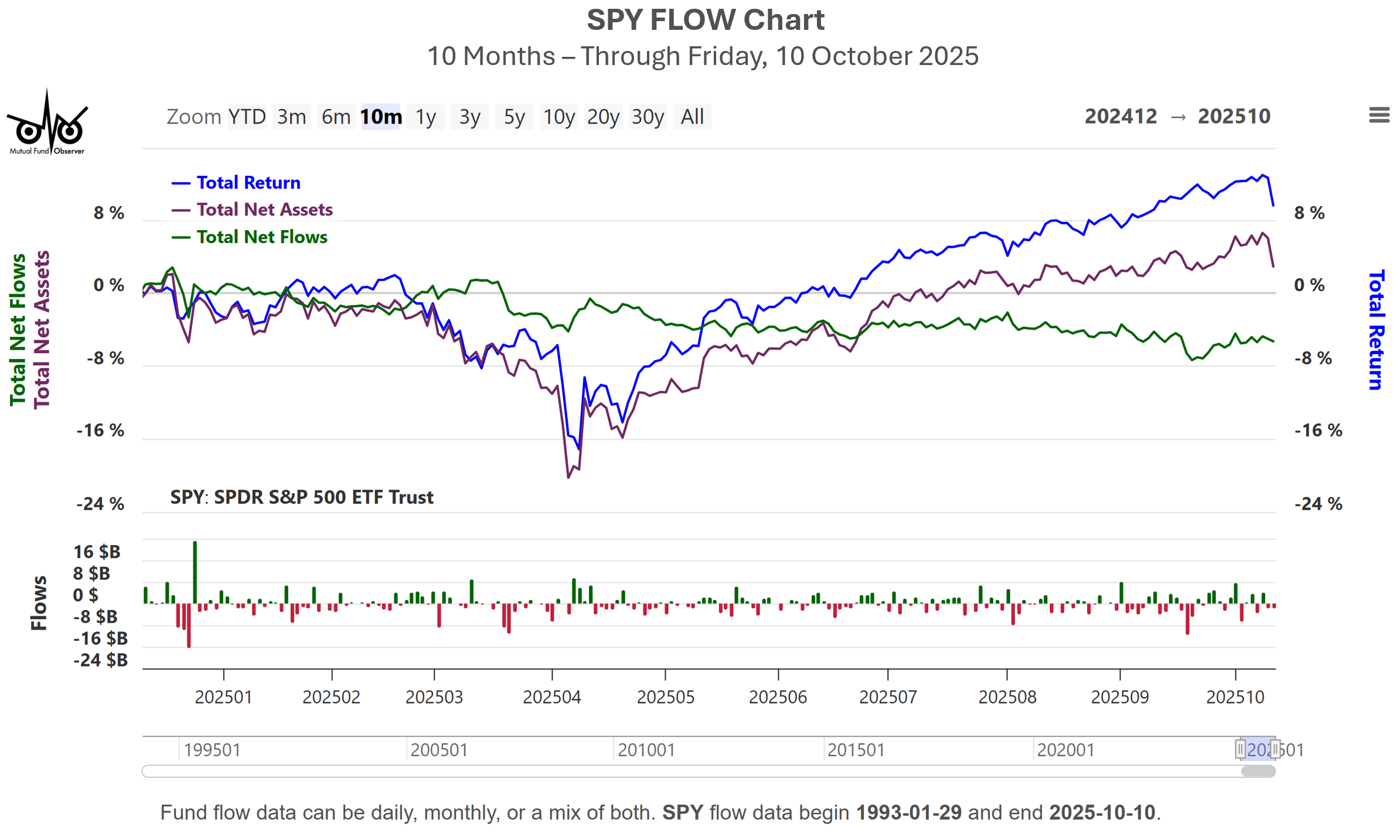

+1Unlike April, bonds behaving normally again, seems like. After Friday's swoon, SPY -2.7% (QQQ -3.5%), pretty massive, as @Junkser points out. But TLT up an impressive 1.6%.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla