It looks like you're new here. If you want to get involved, click one of these buttons!

Still available - looks like 3,325 left.Jonesboro State Bank CDs are all gone? Yields of both CD and treasury are going up.

Binance, the world’s largest cryptocurrency exchange, may have lost half a billion dollars after a hack of its network.

The company temporarily suspended transactions and the transfer of funds after detecting an exploit between two blockchains, a method of digital theft that has been used recently in at least one other major hack.

“The issue is contained now. Your funds are safe. We apologize for the inconvenience and will provide further updates accordingly,” Binance’s CEO, Changpeng Zhao, said in a tweet.

Binance originally said that $100m to $110m in funds were taken. Since then, CNBC has reported the crypto company has lost $570m.

In a blogpost on Friday, Binance said it was working on locking down any areas of vulnerability. “First, we want to apologize to the community for the exploit that occurred. We own this,” the company wrote. “Thanks to the assistance of all the security experts, projects, and validators, the vast majority of the funds remain under control.”

Last year Binance said that it was time for global regulators to establish rules for crypto markets. The company acknowledged at the time that crypto platforms have an obligation to protect users and to implement processes to prevent financial crimes, along with the responsibility to work with regulators and policymakers to set standards to keep users safe.

Binance is just the latest crypto company to experience a targeted hack. In August Nomad, a service that allows users to send crypto tokens between different blockchains, was struck, with media reports saying it was taken for nearly $200m. Harmony, another transfer service, lost about $100m in a hack in June.

Associated Press contributed to this article

Wait....is 'covenant-lite' loans essentially a modified version of NINJA loans? Yikes, they never learn, do they.I disagree that only those who didn’t need money got low rate loans:

https://spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/high-yield-bond-and-leveraged-loan-sales-top-1-trillion-in-2021-67670013

For investors as opposed to the economy—two very different things in 2022–I would say this represents a major fault line: https://spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/covenant-lite-deals-exceed-90-of-leveraged-loan-issuance-setting-new-high-66935148

Anybody heard of or done business with? It's a private Healthcare fund. I can't seem to find anything on them...except from them..ha! Claims good returns but? Any experiences? Thanks

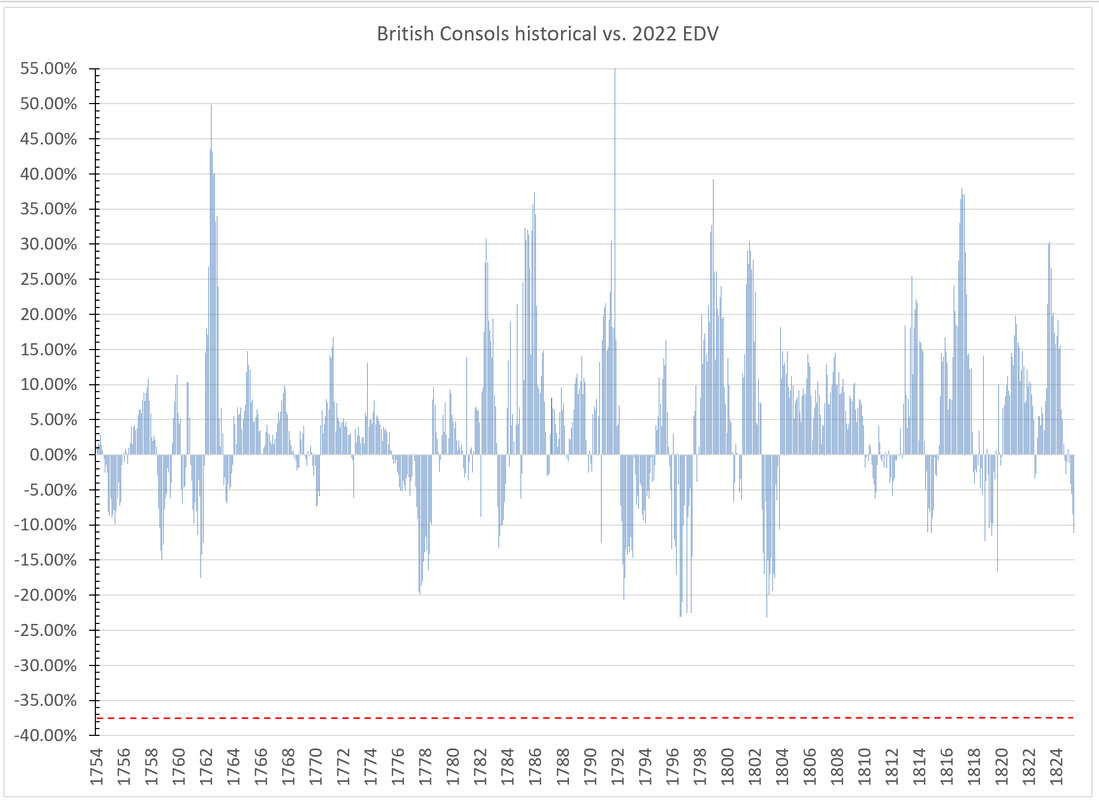

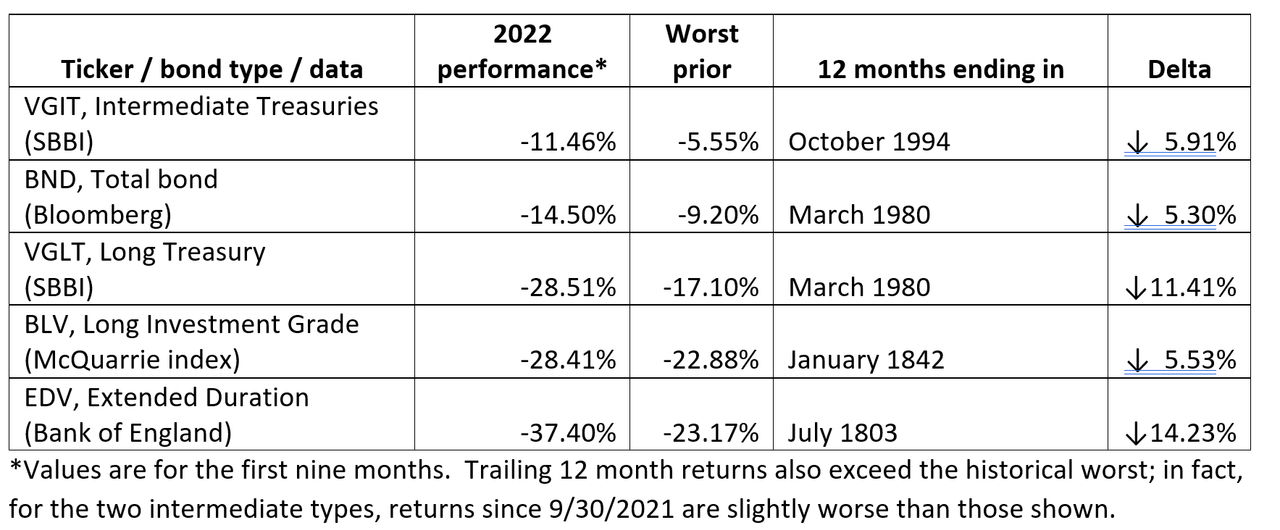

Still a rank newbie here at MutualFundObserver and I will take instruction as to whether it is appropriate to point to related discussions on another forum.Some of these comments make me wonder if the poster read the MW article (Hulbert is a smart and prudent cookie, in my long experience of reading him) , much less the original paper, downloadable here: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4227132 , and hugely sobering if the case.

Dear Anna: you may find this paper reassuring (or not): https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3896672It turns out that deferred accounts are deadly for some widows. The following is an estimate I have made of the federal tax and Medicare B consequences of my husband's death.

Although my income including RMDs from both accounts goes down 19.12%, my taxable income only goes down 8.79% which makes my taxes go up 33.53% landing me in a higher tax bracket.

I'm not sure yet what exactly will happen with Medicare B or when it will happen. As far as I can tell I will, at a minimum, triple my Medicare B premium. It may quadruple if I read the latest table correctly.

Part of the problem is that the Fed hasn’t done what it’s doing now — drastically tightening money to fight inflation — for a long time, indeed since the early 1980s. And some analysts, perhaps including people at the Fed, may have forgotten one important lesson from monetary policy in the bad old days. Namely, it takes a significant amount of time before higher interest rates translate into either an economic slowdown or a drop in the inflation rate.

Consider how Fed policy affects the real economy. One of the main channels is through housing. Higher interest rates lead to reduced demand for houses, which leads to a fall in construction; as incomes earned in housing construction slide, this leads to reduced demand for other goods, and the effects spill over to the economy at large.

But all of this takes a while. The Fed’s rate hikes have indeed led to a sharp fall in applications for building permits. However, construction employment hasn’t yet even begun to decline, presumably because many workers are still busy finishing houses started when rates were lower. And the wider economic effects of the coming housing slump are still many months away.

The other major channel through which the Fed affects the economy is via the value of the dollar. A strong dollar makes U.S. products less competitive on world markets; falling exports and rising imports will eventually be a major economic drag. But it takes time to shift to new suppliers, so this effect won’t really happen until next year.....

....For example, a new report shows that unfilled job offerings fell sharply in August. Why is this important? Many economists — especially economists who have been warning about persistent inflation — argue that the tightness of the labor market is better measured by the ratio of job vacancies to unemployment than by the unemployment rate itself. But this ratio, while still elevated, has already dropped substantially; as Goldman Sachs puts it, almost half of the gap between jobs and workers has been eliminated over the past few months.

Another new report shows that demand for apartments has stalled, which will eventually translate into a decline in rent growth — which basically drives official estimates of the cost of shelter, a key component of most measures of underlying inflation.

Oh, and remember all those supply-chain problems that disrupted the economy and raised inflation some months back? Well, the cost of shipping a container across the Pacific, which was $20,586 in September 2021, is now $2,265.

I’d argue that these indicators tell us that the Fed has already done enough to ensure a big decline in inflation — but also, all too possibly, a recession.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla