Dear friends,

aAugust, famously “summer’s last messenger of misery,” is upon us. It’s a month mostly celebrated by NFL fans (for the start of training camp and the endless delusion that this might be the year) and wiccans (who apparently have a major to-do in the stinkin’ heat). All of us whose lives and livelihoods are tied to the education system feel sympathy for the poet Elizabeth M. Taylor:

August rushes by like desert rainfall,

A flood of frenzied upheaval,

Expected,

But still catching me unprepared.

Like a match flame

Bursting on the scene,

Heat and haze of crimson sunsets.

Like a dream

Of moon and dark barely recalled,

A moment,

Shadows caught in a blink.

Like a quick kiss;

One wishes for more

But it suddenly turns to leave,

Dragging summer away.

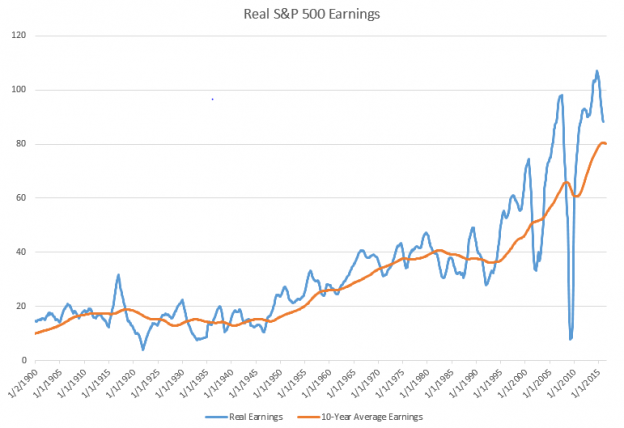

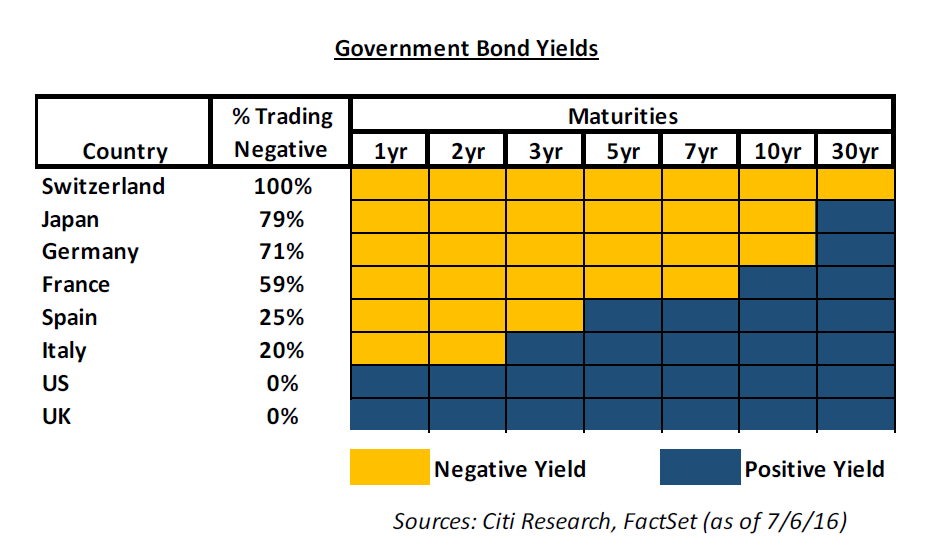

I could, I suppose, grumble again about the obvious (the combination of repeated stock market records with withering corporate fundamentals isn’t good), but Ed bade me keep silent on the topic. So we’ll try to offer up a bunch of lighter pieces, suitable to summer. Continue reading →