Stan Druckenmiller (June 2022)

Some poster on YT did a more detailed summary than did I:

2:11 In my career I've said many things that didn't turn out

4:00 The last 10 or 11 years we've had $30 trillion in QE

4:35 This business is about guessing

5:11 We've only pulled off 2 or 3 soft landings in history. The one I remember was 1994/1995

5:20 We've never had a soft landing after inflation has gotten above 4.5%

5:56 Anything is possible. I've been wrong plenty of times in my career

6:25 Once inflation has gotten above 5%, it's never come down unless Fed Funds has gone above CPI

(but this time that will probably be broken, because Fed Funds would have to go above 8% this time)

7:24 Once inflation has gotten above 5%, it's never been tamed without a recession

8:23 We have $1 trillion to $1.5 trillion in excess savings (who? households or the Government?)

9:53 I was a dropout of a Ph.D program at the University of Michigan

9:57 I don't use what traditional economists use to predict the economy -- things like employment

10:17 The inside of the stock market has a prescient message regarding future economic activity

10:27 Stocks lead fundamentals by 6 to 12 months

11:00 We listen to companies and do a bottom-up analysis

11:14 If leading industries are turning up or down, that's a signal

11:27 The bond market used to be a prescient signaler,

but the last 10 or 11 years it hasn't signaled because the Central Banks have manipulated bond prices

12:04 Last summer when the 10-year yield dropped from 1.70 to 1.15, I didn't anticipate that

12:15 Central banks were buying trillions of dollars and manipulating price of bonds

13:15 Home builders with good fundamentals have declined 50% from their highs (might actually be around 36% drop)

13:28 Trucking is down 40% from their highs (might actually be around 30%)

13:49 Retail numbers are tainted. Can't just accept them blindly

14:48 A lot of these signals have long lead times, 6 months to a year (meaning, recession might not happen until 6 months to a year)

16:10 When I first got into the business,

if a company reported bad earnings but still closed the day positive, that stock was going to be up 6 months from then (and vice versa)

16:28 If the economy looked great and bonds were rallying, that meant the economy was not going to be great

16:55 Price versus news is weakened these days compared to 20 years ago

17:21 I started in this business in the mid 1970s

17:27 Traditionally, I learned that during bear markets I had to morph into bonds, commodities, foreign currencies

17:45 Maybe this says something about my dysfunctional personality but I've always made more money during bear markets

17:55 the way I did it was by ignoring equities and taking them off the table, and buying bonds

18:00 But I've never seen a situation like this where inflation is over 8% and yields 3%

18:21 Referring to golf, I feel like I'm about to play without a driver or wedge, because bonds which have been my go-to may not work this time

18:50 Investing is an art form and you have to innovate from cycle to cycle

20:29 I've lived through enough bear markets to know that if you get aggressive shorting, you can get your head ripped off with rallies

21:03 Side-stepping a decline is not the worst thing in the world (that is, getting out rather than risking losing or gaining)

21:31 I'll be surprised if sometime in the next 6 months the dollar DOESN'T weaken

23:09 There's a strong correlation between crypto and NASDAQ

24:00 My 69th birthday is in a few weeks

24:32 I feel like my predictive power is better but I'm not making as much money because I'm not as aggressive (with investing)

26:34 If we're gonna have a bull market, I want Bitcoin. If we're gonna have a bear market, Gold

27:35 You gotta know your own biases

28:10 I was lazy in college, but I'm passionate about investing.

I'm intellectually stimulated imagining the world and prices 12 to 18 months from now

31:15 Business school says that if you're highly diversified, you have less risk. I don't believe that at all

31:26 People get in the most trouble when they have stale longs or shorts

31:42 You have to have ruthless discipline and be paranoid

32:09 What I learned from George Soros is that it's not about whether you're right or wrong,

it's about how much you make when you're right and how much you lose when you're wrong

32:25 I believe in streaks. One of my number 1 jobs is to know when I'm hot or cold

35:41 When you hear a good idea, within 2 or 3 weeks it may be too late

Stan Druckenmiller (June 2022) Excellent post. Thank you for summarizing. Druck’s a smart dude. I can’t argue with similarities to the 30s. My money is still on the “Fed Put” this time around. But a close call. Something else I don’t see mentioned in the media is the possibility of a “Double Dip”. Perhaps a mild recession and brief “recovery” followed 6-months to a year later by a brutal recession / depression as the Fed resumes tightening. I’d say that’s a 1 in 5 probability - but shouldn’t be dismissed.

Not to monopolize here, but I do suspect the “free-fall” in many commodities today has gotten the Fed’s attention.

Stan Druckenmiller (June 2022) A recent (June 2022) , long-format discussion with Stan Druckenmiller.

Some key takeaways: (paraphrasing)

-Historically, he (Stan) made more money in bear markets, not bull markets -- because he could load up on 'safe' bonds and let the Central bank lower rates.

-Historically when interest rates, oil, and the DXY (USD) are all up, company earnings -- and stock prices head down. Stan asks: Does this sound like today?

-He has less high conviction bets than he normally does. His current bets elicit humility on his part.

-If a strong equity rally (

15% or so) were to follow, he would be inclined to short it at that point.

-Still likes energy fundamentals (supply/demand). But concerned the trade is crowded

-No historic analog for our current (macro-) circumstances (esp. as regards Central banks) but, the possibility of the

1930's comes close).

Falling Commodity Prices Raise Hopes That Inflation Has Peaked One commodity with the potential for price pressure for an extended period of time....

“This is the 1970s for natural gas,” says Kevin Book, managing director at ClearView Energy Partners LLC, a Washington-based research firm. “The world is now thinking about gas as it once thought about oil, and the essential role that gas plays in modern economies and the need for secure and diverse supply have become very visible.”

Natural Gas Soars 700%, Becoming Driving Force in the New Cold War

Midyear Investing Outlook: Where to Invest Now

I don't base my investing decisions on actions taken by momentum traders.

Regardless of how astute they claim to be.

Which brings to mind, why do certain investors feel obliged to frequently post

select trades on various anonymous investing forums?

Would this count as an anonymous investing forum? Which others are you talking about Observant

1?

“Everything we deal with is significantly cheaper than it was six - 12 months ago.” - Howard Marks Link to Oaktree Capital for those interested in investing with Howard Marks

https://www.oaktreecapital.com/(Minimum investment for individuals is generally $

100 Million.)

“Everything we deal with is significantly cheaper than it was six - 12 months ago.” - Howard Marks From this week’s Barron’s:

“Today I am starting to behave aggressively. Everything we deal with is significantly cheaper than it was six to 12 months ago.” - Howard Marks, Oaktree Capital

There was no accompanying article in

Barron’s. The interview they were referencing appears to have been published in the

Financial Times. I’m unable to access it.

I never felt Marks was telling you and me to start buying risky assets. Running a large investment company is much different than levering your family’s life savings.

Thanks

@Junkster for the comments. +

1I’ll try to draw from original sources in the future. My thoughts are that Marks doesn't customarily dish-out investment advice to others. He runs his own ship and discusses his own methods and philosophy. I think trying to take instruction from him would be difficult. Personally, I love reading and learning about investing. It’s not important to me whether or not “actionable advice” can be gleaned from a source. But, others differ in expectations.

“Everything we deal with is significantly cheaper than it was six - 12 months ago.” - Howard Marks Howard Marks specializes in distressed debt ala junk bonds, bank loans, etc. Over the past several months I have continually read about how junk bonds offer value from various pundits. All the while it is one new low after another for junk bonds. So much so that the first half decline of

14% was the worst first half decline ever for the junk bond market.

What is particularly ominous is how detached junk bonds have been from equities and Treasuries. Meaning while equities had a vicious bounce a few weeks ago, junk and bank loans just kept making new lows. While Treasuries are having a nice recovery presently still new lows in the risk on credits aka junk and and bank loans. Below is a link to Morgan Stanley’s outlook for junk. Sounds much more objective and reasoned than much of what I have read recently

https://www.zerohedge.com/markets/morgan-stanley-recession-arrives-will-we-see-surge-corporate-defaultsEdit: Obviously as with Treasuries recently, these markets can turn on a dime. And junk bonds are notorious for strong recoveries after bear declines. Coming off the 2008 bear market in

2009 junk had the greatest credit rally of all time rising over 50%.

Edit: Today’s action in junk bonds so far at least so far not as negative as it may appear. Although down, the junk ETFs are still trading well above Friday’s NAV meaning the open end may be up today.

Falling Commodity Prices Raise Hopes That Inflation Has Peaked Oil’s off 8.4% in late morning trading. Under $100. Good news.

“Everything we deal with is significantly cheaper than it was six - 12 months ago.” - Howard Marks Wasn't Howard Marks gloating in 2021 that although he personally missed the boat on cryptos, his son Andrew, who now manages family accounts, was into cryptos, and that Marks was gaining a new appreciation for Bitcoin, especially because of its limited supply. I thought at the time that must be something when a diehard value guy like Marks started to sing praises of Bitcoin. I think that Marks also mentioned this in one of his essays.

Matthews Asia ETFs in registration

Falling Commodity Prices Raise Hopes That Inflation Has Peaked

Falling Commodity Prices Raise Hopes That Inflation Has Peaked Excerpt from a WSJ article (on Apple News) that inflation may be cooling.

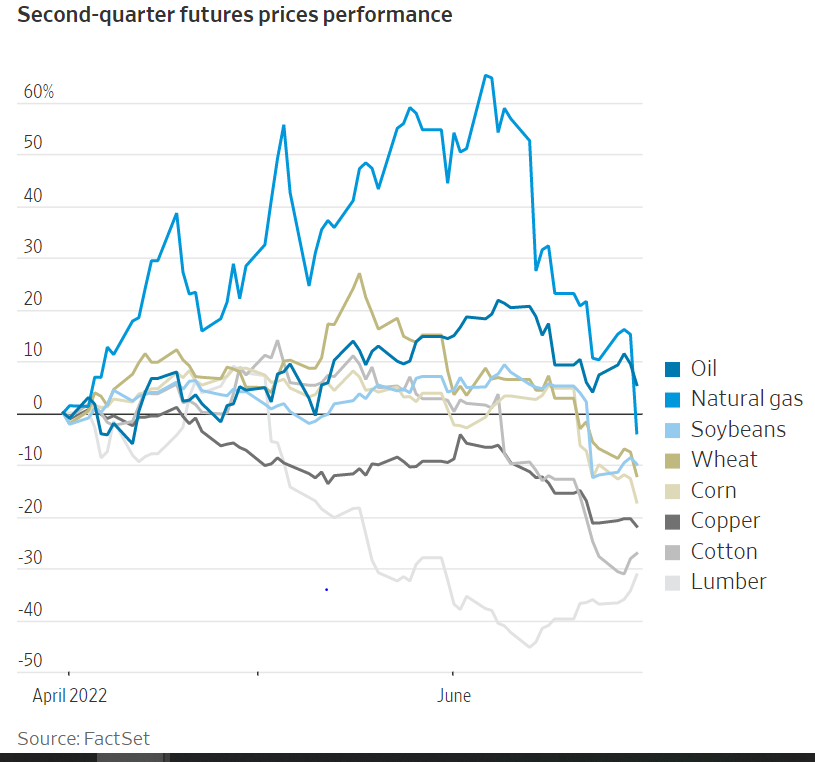

Natural-gas prices shot up more than 60% before falling back to close the quarter 3.9% lower. U.S. crude slipped from highs above $120 a barrel to end around $106. Wheat, corn and soybeans all wound up cheaper than they were at the end of March. Cotton unraveled, losing more than a third of its price since early May. Benchmark prices for building materials copper and lumber dropped 22% and 31%, respectively, while a basket of industrial metals that trade in London had its worst quarter since the 2008 financial crisis

This accounted for recent decline in commodity and commodity futures funds and ETFs.

Money Market Rates - interesting again? "all wires are subject to a wire fees

Some brokerages may waive the fee if your account is large enough. Schwab waives its fee for the first three wires per quarter if you have $

100K with them.

https://www.schwab.com/legal/schwab-pricing-guide-for-individual-investors"

I have never done a wire into or out of Schwab before. This is the first time I took money out of Schwab. My household balance at Schwab has been way more than the $

100K requirement posted at the link - I am happy to share with

@Yogibearbull if anybody doubts. Life is too short for me to go back and dispute with Schwab about their advice. As I said, I do not pay wire fees at other brokerages. I mentioned to Fidelity about my interaction with Schwab regarding the wire, and Fidelity claimed they do not charge for any outgoing wire for any client. There was no reason for me to check their fees schedule. Please check if it is relevant for you.

Money Market Rates - interesting again? The incremental yield between SPAXX and FZDXX is about 40 basis points (0.99% vs

1.40% SEC yield as of June 30th). And as

@BaluBalu noted, you don't have to move money out of FZDXX to write a check. So you get that extra 40 basis points for weeks, if not months. At least assuming that the gates are not triggered.

(They have not yet been repealed; the SEC has yet to issue its Final Rule. I checked before making my prior post.)

Swing pricing is proposed only for institutional prime funds. Rather than eliminating the distinction between institutional and retail funds, this would amplify it. And it is this part of the proposal that has drawn the most negative feedback.

Due to differences in observed investor behavior and liquidity costs during a crisis among the various fund types, swing pricing would not apply to government money market funds or retail money market funds.

https://www.sidley.com/en/insights/newsupdates/2022/01/sec-proposes-new-rule-amendments-for-money-market-funds

Money Market Rates - interesting again? While it is true that prime m-mkt funds haven't had to impose gates/redemption fees, the latest m-mkt reforms are driven by the fact that 2014/2016 m-mkt rules (that had gates/redemption fees for prime m-mkt) decimated prime m-mkt funds in 2020 and other later times by huge outflows just from the fears of possible gates/redemption fees. This was so bad that it destabilized the commercial paper market. I haven't kept track of these latest m-mkt reforms but I recall that the idea was to do away gates/redemption fees in the favor of floating NAVs for all prime funds (thus eliminating distinctions between retail and institutional prime).

IMO, the small incremental yields offered by prime m-mkt funds aren't worth the associated headaches. This is especially so if check-writing is involved and some checks can remain outstanding for weeks, if not months.

Money Market Rates - interesting again?

Midyear Investing Outlook: Where to Invest Now I don't base my investing on outlooks or prediction, it's based on big picture + several indicators (

link). Both signaled high risk months ago and why I'm in MM since then with only short term trades if the charts support it. It's not the first time. I sold before 03/2020(this post is from 2/29/2020(

link) and Q4/20

18 and bought back much lower after risk was lower.

I don't base my investing decisions on actions taken by momentum traders.

Regardless of how astute they claim to be.

Which brings to mind, why do certain investors feel obliged to frequently post

select trades on various anonymous investing forums?