It looks like you're new here. If you want to get involved, click one of these buttons!

Thanks for your information Hank! Your comparisons are actually to those of "bee", which I quoted in my post to you above, but that is fine since this thread actually should link back to the OPs.”hank, are you willing to provide more personal details about your situation, so your opinions have some context?”

Which opinion? I’ll try to compare my situation to yours but not sure if that affects most of my opinions about investing or finance..

- “When I retired 13 years ago,”

I retired 25 years ago

- ”I attempted to project my future spending needs”

Ditto. I worked this out over the 2 or 3 years before retiring.

- “Over these years I have meet my spending needs with a combination of pension income (with a COLA), an Annuity Income (Savings that I converted to an Annuity), and some part time work.”

Pretty close. I have Social Security and a pension. While working I opted-in to a pension feature that adds 3% yearly of initial amount. Not really COLA - but helpful. The pension provides some supplemental health care coverage in combination with Medicare. I’m not as up-to-speed as I should be on the out-of-pocket expenses - but there are some. Never owned an annuity. No part time work. Active maintaining home infrastructure others might farm out.

- ”Since retirement, I have continue to contribute to my HSA and my IRA with contributions from part time work income. Recently I began managing one of my properties as a seasonal rental for additional income. I will work part time spending some of that work income and saving some into an IRA until age 73. My RMDs will then become a forced taxable event that may turn into an income source if needed or taxable savings if not needed."

Had a 403-B at work invested 100% in a global equities for 28 years. On retirement I converted it to a Traditional IRA and diversified the assets more broadly. In early ‘09 I converted about 40% to a Roth to take advantage of the crash. Made 2 smaller conversions over the next decade. 90% now in a Roth. RMDs alone from the Traditional are adequate to meet all my needs (along with SS & pension). The Roth provides a safety-net that might be needed for major infrastructure repair or other unexpected needs. I’m single and once-divorced. Own some nearby real estate that could be sold for additional cash. The home has a small fixed rate 3.13% mortgage (less than 20% of value) taken out for some renovation more than 5 years ago. Could pay it off, but think I can do better investing across a diversified portfolio consisting largely of OEFs, CEFs & ETFs.

Barron's, Vanguard Throws in the Towel on Its Managed Payout Fund, Feb 28, 2020Payout funds got their start during the 2007-2008 financial crisis when Vanguard and Fidelity both launched the products. The idea was appealing: Convert a retirement savings pool into a reliable income stream and offer investors peace of mind that they’d get a monthly paycheck, regardless of the market’s ups and downs.

...

Vanguard initially had three payout funds but merged them into one fund in January 2014. Fidelity developed a series of Income Replacement funds, paired with an optional monthly payout feature, but Fidelity rebranded the funds in 2017 as “Managed Retirement Income” with more of a high-income focus rather than managed payouts.

One hurdle: Managed payout funds have long had trouble hitting their income targets without dipping into capital—simply giving investors part of their money back. Annuities work similarly, though they have an insurance component that can keep the income flowing if the portfolio runs out of money.

What annuities do is pool risk. Some people die early, others later. Instead of each individual self insuring (collectively overinsuring), individuals pool their risk through an insurance company. This provides larger income streams safely.[U]sing a relatively simple model we estimate consumption could increase by approximately 80% for retirees if assets were converted to lifetime income streams, where the improvement rates are significantly higher for joint households

The Mechanics and Regulation of Variable Payout Annuities (50 pages. TL;DR)Variable payout annuities provide protection against longevity risk and allow for some participation in the higher (but more volatile) returns of corporate equities and other real assets. They also avoid the annuitization risk because their benefit payments vary with investment performance and are not fully determined by the prevailing conditions at the time of retirement. But VPAs are exposed to investment and inflation risks ...

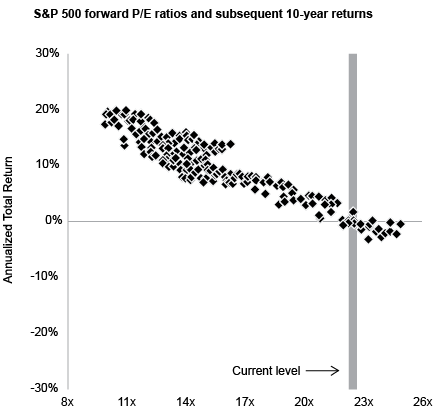

Very Interesting Article and Video Presentation.Michael Cembalest is the Chairman of Market and Investment Strategy at JP Morgan Asset Management.

Since 2005, Michael has been the author of the Eye on the Market, which covers a wide range of topics across markets, investments, economics, politics, energy, municipal finance and more.

For 2025:

Deregulation, deportations, tariffs, tax cuts, cost cutting, crypto, oil & gas, medical freedom and Agency purges: What could possibly go wrong?

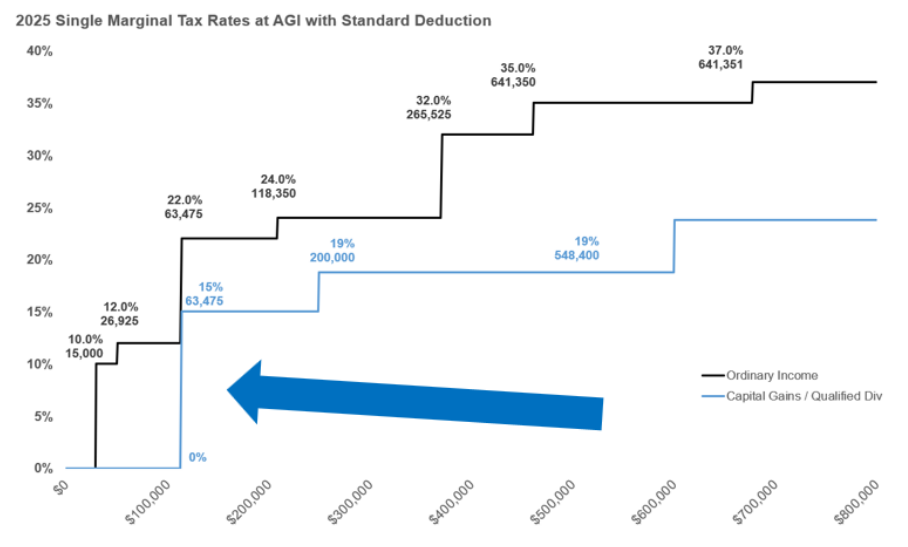

For 2024, individuals with taxable income below $47,025 ($94,050 for married couples) pay 0% tax for long-term capital gains (LTCG). In years when you’re under the threshold you could effectively lock in tax-free long-term gains. The idea would be to realize just enough LTCG to stay within the 0% tax bracket. You also have to tack on the standard deduction which is $15,000 for individuals or $30,000 for a married couple. That means don’t have to pay federal income taxes on your long-term capital gains until your income exceeds a little more than $63,000 (single) or $126,000 (married couple). So you could realize more than $63,000 ($126,000) in capital gains and dividends without paying any federal income tax.

Their 19(a) filing from December@rforno: I can't locate any info on that UTG 60% ROC. Do you have a source?

If you like the sector and the managers take a look at UTES. However if it's the income you were after don't bother. DNP might be an income source.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla