A tradition dating back to the days of FundAlarm was to annually share our portfolios, and reflections on them, with you. My portfolio, indolent in design and execution, makes for fearfully dull reading. That is its primary charm.

This is not a “here’s what you should own” exercise, much less an “envy me!” one. Instead, it’s a “here’s how I think. Perhaps it will help you do likewise?” exercise.

My portfolio and my life

By design, my portfolio is meant to be mostly ignored for all periods because, on the whole, I have much better ways to spend my time, energy, and attention. For those who haven’t read my previous discussions, here’s the short version:

Stocks are great for the long term (think: time horizon for 10+ years) but do not provide sufficient reward in the short term (think: time horizon of 3-5 years) to justify dominating your non-retirement portfolio.

An asset allocation that’s around 50% stocks and 50% income gives you fewer and shallower drawdowns while still returning around 6% a year with some consistency. That’s attractive to me.

“Beating the market” is completely irrelevant to me as an investor and completely toxic as a goal for anyone else. You win if and only if the sum of your resources exceeds the sum of your needs. If you “beat the market” five years running and the sum of your resources is less than the sum of your needs, you’ve lost. If you get beaten by the market five years running and the sum of your resources is greater than the sum of your needs, you’ve won.

That might be the single most important perspective you can take away this month. Investing is about having reasonable security in support of a reasonably rich life. Not yachts. Not followers. Not bragging rights. Life.

“Winning” requires having a sensible plan enacted with good investment options and funded with some discipline. It’s that simple.

My portfolio is built to allow me to win. It is not built to impress anyone.

My asset allocation decisions

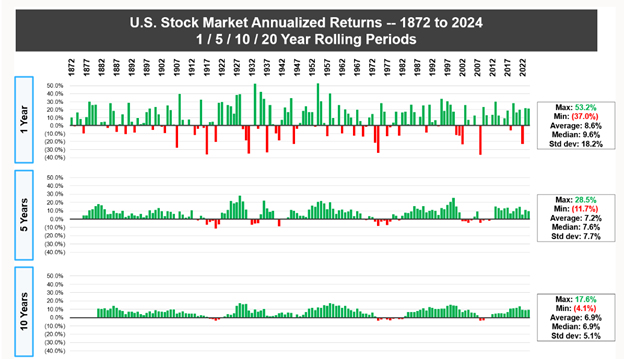

Stocks are rewarding in the long run, gut-wrenching in the short run, and frequently miserable disappointments in the medium run. The “miserable – medium” sentence translates to this: it is painfully common for the stock market to go 5 – 10 years without a gain. A Canadian financial education site, A Measure of a Plan, offered this 150-year chart of US market performance.

So, on a rolling basis, there appear to have been 14 decade-long periods and two dozen five-year periods in which investors made no money. On the whole, I would prefer steady gains to mixing spectacular gains, sickening losses, and years of futility. That led me to an unconventional asset allocation: 50%.

“50% what?” you ask. 50% everything. My portfolio targets 50% equity and 50% not, which translates to 50% growth and 50% stability. My equity portfolio targets 50% US and 50% not. My stability portfolio targets 50% bonds and 50% not.

That’s based on a lot of research from T. Rowe Price on the return/volatility tradeoff as portfolios increase their exposure to stocks. Short version: you pay a very high price in the short- to medium-term for a prospective gain of two or three percent in returns. A 50% portfolio offers the prospects of returns of 6-7% on average with a small fraction of the market’s downside. That works for me.

My year-end 2024 allocation

| Domestic equity | Close enough | Traditional bonds | Nailed it |

| Target 25% | 2024: 23% | Target: 25% | 2024: 25% |

| Also managed a 50% large-cap / 50% small to mid-cap weight. | Surprising sources: Palm Valley Capital is 30% short-term bonds | ||

| International equity | Overweight | Cash / market-neutral / liquid | Close enough |

| Target 25% | 2024: 31% | Target: 25% | 2022: 22% |

| This has been a pretty long-lasting overweight. The average US investor has 15% of their equities in international stocks while I’m targeting 50% and sitting at 60%. | Rather a lot of my managers have found reason to hold a lot of cash of late. FPA, Leuthold, and Palm Valley all sit at or above 20%. | ||

Here’s what that looks like in terms of performance and volatility.

| Annual return | Max Loss | Standard Deviation | Sharpe Ratio | Ulcer Index | |

| 2024 | 6.7 | -2.0 | 5.3 | 0.32 | 0.9 |

| Three year | 2.7 | -16.2 | 9.4 | -0.14 | 6.9 |

| Five year | 7.1 | -17.6 | 11.1 | 0.42 | 6.6 |

The three-year performance looks bad because it includes 2022 when the stock market dropped 23% and the bond market fell 13%. The Indolent Portfolio did better than either in 2022 and about 4% better than a hypothetical portfolio with the same weightings. And that’s been true most years: 1-2% better than a peer-weighted portfolio, 6-9% returns, volatility in check.

My investment choices

I own 11 funds. Yes, I know that’s more than I need. Some of the sprawl represents my interest in tracking newer and innovative funds, some represent a tax trap (I have a lot of unrealized gains) and some is indolence. A fund is doing fine, so why bother to change?

In general, my core funds are equity-oriented but the managers have the freedom (and the responsibility) to invest elsewhere when equities are not offering rewards that match their risks.

Core growth funds – 2024

| Weight | APR | Max Loss | Standard Deviation | ||

| FPA Crescent | Flexible Portfolio | 22% | 14.0 | -2.0 | 6.1 |

| Palm Valley Capital | Small-Cap Growth | 8% | 4.2 | -0.4 | 0.0 |

| Leuthold Core Investment | Flexible Portfolio | 6% | 7.7 | -5.0 | 10.3 |

| Brown Advisory Sustainable Growth | Multi-Cap Growth | 6% | 20.2 | -5.5 | 12.0 |

Leuthold and FPA are two very different versions of disciplined “go anywhere” funds; each seeks equity-like returns with sub-market risk. Leuthold is a quant fund, and FPA’s bias is “absolute value.” Palm Valley Capital is the fourth incarnation of Eric Cinnamond’s strict small-cap discipline: he loves great stocks but would rather sit on hot coals than buy stocks that aren’t priced for exceptional gains. Lots of cash for long periods, which is frustrating for some and just fine for me. Brown Advisory was my choice for the best sustainable equity fund I could find. Their attention to quality and valuations was negative in 2024.

Core income / market neutral funds – 2024

| Category | Weight | Return | Max loss | |

| T Rowe Price Multi-Strategy Total Return | Alternative Multi-Strategy | 10.0% | 5.3 | -0.7 |

| T Rowe Price Spectrum Income | Multi-Sector Income | 5.0% | 4.0 | -1.6 |

| RiverPark Strategic Income | Flexible Portfolio | 8.0% | 8.2 | 0.0 |

| RiverPark Short Term High Yield | Short High Yield | 8.0% | 5.3 | 0.0 |

Multi-Strategy is Price’s version of a hedge fund for the common investor. It’s growing on me with a low correlation to the market, and low downside capture. Spectrum is a fund-of-income fund. And the two RiverPark funds are low-risk, credit-oriented investments. Short Term made money in 2022 when everything else faltered.

That whole “international overweight” thing – 2024

| Category | Weight | Return | Max loss | |

| Seafarer Overseas Value | International Small / Mid-Cap Value | 4.0% | -3.3 | -7.3 |

| Grandeur Peak Global Micro Cap | Global Small- / Mid-Cap | 14.0% | 3.2 | -6.0 |

| Seafarer Overseas Growth and Income | Emerging Markets | 9.0% | -5.4 | -9.2 |

In general, I’ve never understood why buying shares of large multinational corporations nominally headquartered in London would logically produce results different from buying shares of large multinational corporations nominally headquartered in Boston. As a result, my impulse was to look at smaller markets and smaller companies. In theory, that should work splendidly. In practice, it’s so-so.

Alternatives to my choices

It’s not necessary to own more than two or three funds to create an indolent portfolio. The key choice is whether you want to build substantial cash (or cash-like securities) into the mix or stick with stocks and bonds alone.

The Bogleheads endorse a three-fund portfolio which does not consider “cash” to be an investment. Their process has two steps: (1) pick the asset allocation that’s right for you and (2) buy three low-cost index funds that give you exposure to the assets you’re seeking. Their default set is:

- Vanguard Total Stock Market Index Fund (VTSAX)

- Vanguard Total International Stock Index Fund (VTIAX)

- Vanguard Total Bond Market Fund (VBTLX)

Step One – “figure out your asset allocation” – is the tricky one there. A very simple two-fund portfolio – one flexible fund in the hands of a top tier manager and one incoming producing fund similarly skippered – split 50/50 could replicate my portfolio and would require negligible maintenance.

The small investor’s indolent portfolio

| Lipper Category | Weight | APR | Max Loss | |

| Portfolio | – | 100.0% | 6.8 | -2.2 |

| RiverPark Short Term High Yield | Short High Yield | 50 | 5.3 | 0.0 |

| Leuthold Core Investment | Flexible Portfolio | 50 | 7.7 | -5.0 |

Alternately …

| Lipper Category | Weight | APR | Max Loss | ||

| Portfolio | – | 100.0% | 11.1 | -0.9 | |

| FPA Crescent | Flexible Portfolio | 50.0% | 14.0 | -2.0 | |

| RiverPark Strategic Income | Flexible Portfolio | 50.0% | 8.2 | 0.0 | |

Bottom Line

The best portfolio, like the best water heater or best car, is the one that you never need to think about. My portfolio assumes a balanced allocation with the average fund being in the portfolio for more than a decade. That strategy doesn’t make me rich, it makes me happy. And that’s rather the goal!