On August 3, 2021, Virtus Partners launched their latest collaboration with Kayne, Anderson, Rudnick (KAR), Virtus KAR Small-Mid Cap Value. The fund is managed by the KAR of the title: Kayne, Anderson Rudnick Investment Management, Virtus’s largest wholly-owned subsidiary. KAR, based in Los Angeles, manages rather more than $17 billion in assets.

Across all of their portfolios, KAR emphasizes one core attribute:

It has generally worked well for them. The KAR Small Cap Core, Small-Mid Cap Core, Small-Mid Cap Quality Value, and Mid Cap Core portfolios all received the Manager of the Decade designation from Informa Investment Solutions for the 10-year period ending December 31, 2019. Informa is a financial intelligence firm that caters to institutional investors.

In particular, it will be managed by Julie Kutasov and Craig Stone, the same team responsible for Virtus KAR Small-Mid Cap Core and Virtus KAR Small Cap Value.

What will they do?

The plan is to build a portfolio with three characteristics:

High-Quality Businesses

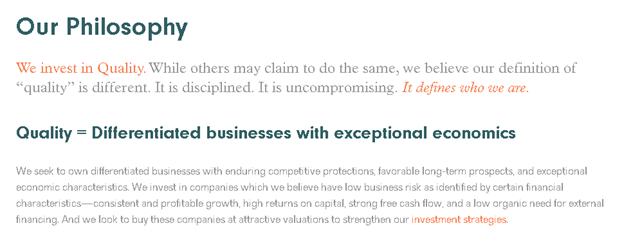

Searches for quality small-mid capitalization value companies with solid balance sheets, consistent growth, profitability, and market-dominant business models.

Lower Volatility Approach

Extensive fundamental research favors companies with less business risk, as defined by lower earnings variability, consistent and profitable growth, high returns on capital, strong free cash flow, and a low organic need for external financing, all of which can help to protect profits in difficult markets.

High-Conviction Portfolio

Focused on the portfolio team’s 25-35 strongest investment opportunities, with a long-term, low-turnover approach to realize full stock value potential.

Compared to their Morningstar peers, the team’s Small Cap Value fund has below average standard deviation and beta, a “low” risk score, and a substantially higher quality portfolio (measured by the percentage of stocks with a “moat,” financial health, and profitability). The portfolio holds 31 stocks, with a 19% turnover ratio (which is exceedingly low), and an active share of 96 (which is exceedingly high).

The fund had strong absolute returns in 2020, but weak relative ones, and that lag weakens its long-term performance record.

The Virtus KAR Small-Mid Core Fund has a shorter, stronger record but, by Morningstar’s calculation, is most heavily invested in mid-cap growth stocks.

Bottom line: Kutasov and Stone benefit from KAR’s strong culture and deep bench. That said, they seem to be modestly more adept at selecting somewhat larger and somewhat growth-ier stocks. This is likely to be a solid performer with subdued risk and a mid-cap bias.

“A” shares of the new fund have a 1.17% expense ratio. The minimum initial investment nominally is $25,000, but it’s available at TD Ameritrade (and, presumably, other platforms) for $2,500.

Folks interested in learning more should read KAR’s “Thinking Beyond the Benchmark” (2021), which walks through their review of the Small-Mid Cap Core strategy, including the performance metrics and the underlying rationale for their strategy.