Originally published in October 1, 2013 Commentary

![]()

Portfolio managers Andrew Redleaf and Dr. Jason Cross, along with Whitebox Funds’ President Bruce Nordin, hosted the 2nd quarter conference call for their Tactical Opportunities Fund (WBMIX) on September 10. Robert Vogel, the fund’s third manager, did not participate. The call provided an opportunity to take a closer look at the fund, which is becoming hard to ignore.

Background

WBMIX is the more directionally oriented sibling of Whitebox’s market-neutral Long Short Equity Fund (WBLFX), which David profiled in April. Whitebox is preparing to launch a third mutual fund, named Enhanced Convertible Fund (WBNIX), although no target date has been established.

Whitebox Advisors, founded by Mr. Redleaf in 1999, manages its mutual funds with similar staff and strategies as its hedge funds. Mr. Redleaf is a deep contrarian of efficient market theory. He works to exploit market irrationalities and inefficiencies, like “mispriced securities that have a relationship to each other.” He received considerable attention for successfully betting against mortgages in 2008.

The Tactical Opportunities Fund seeks to provide “a combination of capital appreciation and income that is consistent with prudent investment management.” It employs the full spectrum of security classes, including stocks, bonds, and options. Its managers reject the notion that investors are rewarded for accepting more risk. “We believe risk does not create wealth, it destroys wealth.” Instead, they identify salient risks and adjust their portfolio “to perform at least tolerably well in multiple likely scenarios.”

The fund has attracted $205M AUM since its inception in December 2011 – on the day of the conference call, Morningstar showed AUM at $171M, an increase of $34M in less than three weeks. All three managers are also partners and owners in the firm, which manages about $2.4B in various types of investment accounts, but the SAI filed February 2013 showed none invested in the fund proper. Since this filing, Whitebox reports Mr. Redleaf has become a “significant owner” and that most of its partners and employees are invested in its funds through the company’s 401k program.

Morningstar recently re-categorized WBMIX from aggressive allocation to long-short after Whitebox management successfully appealed to the editorial board. While long-short is currently more appropriate, the fund’s versatility makes it an awkward fit in any category. It maintains two disparate benchmarks, S&P 500 Price Index SPX (excludes dividends) and Barclay’s Aggregate U.S. Bond Total Return Index. Going forward, Whitebox reports it will add S&P 500 Total Return Index as a benchmark.

Ideally, Mr. Redleaf would prefer the fund’s performance be measured against the nation’s best endowment funds, like Yale’s or Havard’s. He received multiple degrees from Yale in 1978. Dr. Cross holds an MBA from University of Chicago and a Ph.D. in Statistics from Yale.

Call Highlights

Most of its portfolio themes were positive or flat for the quarter, resulting in a 1.3% gain versus 2.9% for SP500 Total Return, 2.4% SP500 Price Return, 0.7% for Vanguard’s Balanced Index , and -2.3% for US Aggregate Bonds. In short, WBMIX had a good quarter.

Short Bonds. Whitebox has been sounding warning bells for sometime about overbought fixed income markets. Consequently, it has been shorting 20+ year Treasuries and high-yield bond ETFs, while being long blue-chip equities. If 1Q was “status quo” for investors, 2Q saw more of an orderly rotation out of low yielding bonds and into quality stocks. WBMIX was positioned to take advantage.

Worst-Case Hedge. It continues to hold out-of-money option straddles, which hedge against sudden moves up or down, in addition to its bond shorts. Both plays help in the less probable scenario that “credit markets crack” due to total loss of confidence in bonds, rapid rate increase and mass exodus, taking equities down with them.

Bullish Industrials. Dr. Cross explained that in 2Q they remained bullish on industrials and automakers. After healthy appreciation, they pared back on airlines and large financials, focusing instead on smaller banks, life insurers, and specialty financials. They’ve also been shorting lower yielding apartment REITS, but are beginning to see dislocations in higher yielding REITs and CEFs.

Gold Miner Value. Their one misstep was gold miners, at just under 5% of portfolio; it detracted 150 basis points from 2Q returns. Long a proxy for gold, miners have been displaced by gold ETFs and will no longer be able to mask poor business performance with commodity pricing. Mr. Redleaf believes increased scrutiny on these miners will lead to improved operations and a closure in the spread, reaping significant upside. He cited that six CEOs have retired or been replaced recently. This play is signature Whitebox. The portfolio managers do not see similar inefficiencies in base metal miners.

Large vs Small. Like its miss with gold miners, its large cap versus small cap play has yet to pan-out. It believes small caps are systematically overpriced, so they have been long on large caps while short on small caps. Again, “value arbitrage” Whitebox. The market agreed last quarter, but this theme has worked against the fund since 2Q12.

Heading into 3Q, Whitebox believes equities are becoming overbought, if temporarily, given their extended ascent since 2009. Consequently, WBMIX beta was cut to 0.35 from 0.70. This move appears more tactical than strategic, as they remain bullish on industrials longer term. Mr. Redleaf explains that this is a “game with no called strikes…you never have to swing.” Better instead to wait for your pitch, like winners of baseball’s Home Run Derby invariably do.

Whitebox has been considering an increase to European exposure, if it can find special situations, but during the call Mr. Redleaf stated that “emerging markets is a bit out of our comfort zone.”

Performance To-Date

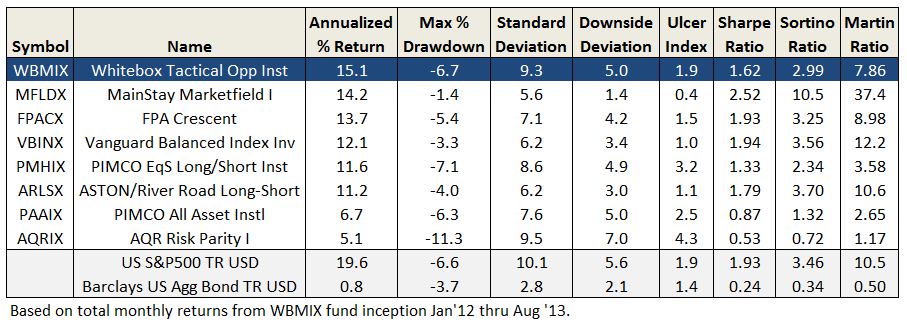

The table below summaries WBMIX’s return/risk metrics over its 20-month lifetime. The comparative funds were suggested by MFO reader and prolific board contributor “Scott.” (He also brought WBMIX to community attention with his post back in August 2012, entitled “Somewhat Interesting Tiny Fund.”) Most if not all of the funds listed here, at some point and level (except VBINX), tout the ability to deliver balanced-like returns with less risk than the 60/40 fixed balanced portfolio.

While Whitebox has delivered superior returns (besting VBINX, Mr. Aronstein’s Marketfield and Mr. Romick’s Crescent, while trouncing Mr. Arnott’s All Asset and AQR’s Risk Parity), it’s generally done so with higher volatility. But the S&P 500 has had few drawdowns and low downside over this period, so it’s difficult to conclude if the fund is managing risk more effectively. That said, it has certainly played bonds correctly.

Other Considerations

When asked about the fund’s quickly increasing AUM, Dr. Cross stated that their portfolio contains large sector plays, so liquidity is not an issue. He believes that the fund’s capacity is “immense.”

Whitebox provides timely and thoughtful quarterly commentaries, both macro and security specific, both qualitative and quantitative. These commentaries reflect well on the firm, whose very name was selected to highlight a “culture of transparency and integrity.” Whitebox also sponsors an annual award for best financial research. The $25K prize this year went to authors of the paper “Time Series Momentum,” published in the Journal of Financial Economics.

Whitebox Mutual Funds offers Tactical Opportunities in three share classes. (This unfortunate practice is embraced by some houses, like American Funds and PIMCO, but not others, like Dodge & Cox and FPA.) Investor shares carry an indefensible front-load for purchases below $1M. Both Investor and Advisor shares carry a 12b-1 fee. Some brokerages, like Fidelity and Schwab, offer Advisor shares with No Transaction Fee. (As is common in the fund industry, but not well publicized, Whitebox pays these brokerages to do so – an expensive borne by the Advisor and not fund shareholders.) Its Institutional shares WBMIX are competitive currently at 1.35 ER, if not inexpensive, and are available at some brokerages for accounts with $100,000 minimum.

During the call, Mr. Redleaf stated that its mutual funds are cheaper than its hedge funds, but the latter “can hold illiquid and obscure securities, so it kind of balances out.” Perhaps so, but as Whitebox Mutual Funds continues to grow through thoughtful risk and portfolio management, it should adopt a simpler and less expensive fee structure: single share class, no loads or 12b-1 fees, reasonable minimums, and lowest ER possible. That would make this already promising fund impossible to ignore.

Bottom Line

At the end of the day, continued success with the fund will depend on whether investors believe its portfolio managers “have behaved reasonably in preparing for the good and bad possibilities in the current environment.” The fund proper is still young and yet to be truly tested, but it has the potential to be one of an elite group of funds that moderate investors could consider holding singularly – on the short list, if you will, for those who simply want to hold one all-weather fund.

A transcript of the 2Q call should be posted shortly at Whitebox Tactical Opportunities Fund.

27Sept2013/Charles