Sussing out publications that cover investments in a fair-minded manner is no easy task. In that light I have been reading Mutual Fund Observer and prior that FundAlarm for as long as I can remember. A monthly publication is for the vast majority of investors as frequent as they need to be checking in on the world of investing.

I also have the benefit of having read both Josh and David’s answers to the question. In that light I will simply agree with what they have both written. I am not sure quite how he does it but Josh has created for himself a process that provides him with what he needs to succeed in a number of different venues. David has correctly noted that a focus on books, not necessarily investment-related, is an important antidote to the daily din of the financial media.

I spend much of my day wading through the financial media and blogosphere looking for analysis and insight that has a half-life of more than a day or two. The recommended sources below do much the same thing with a very different focus.

Print: The Week. You can consume this weekly magazine online but I still rely on the US Mail to provide me with my copy. The Week is a curated look at the week’s, or more likely, the previous week’s news. It covers the gamut from domestic and international news, entertainment, finance and last but not least real estate. The elites may read The Economist every week. Someone with a busy schedule reads The Week.

Podcast: Science Friday. Science Friday is broadcast on many public radio stations but I consume it via podcast. It is already a cliche to say that the worlds of science and technology are changing at an increasingly rapid rate. For a lay audience Science Friday provides listeners with an accessible way of keeping up. For example last week’s show included segments on the science of sunscreen, cephalopod intelligence and 3-D mammography.

Online: The Browser, Longreads and Longform One caveat I would have about reading non-fiction books is that many of them are magazine articles padded out to fill out the publisher’s idea of how long a book should be. If that is the case then reading original long form reporting and analysis should provide us with a good bang for the buck. The Browser is not focused explicitly on long form content, but I thought I would mention it here since it is so darn good.

Successful investing isn’t about making quick decisions in the moment. It is about sitting on your hands most of the time and making decisions after some thoughtful consideration. As I have written prior a multi-disciplinary approach to investing provides you with the perspective necessary to see the world as it is as opposed to how Wall Street would like you to see it.

How I structure my day and set my rules so as to be maximally informed and minimally assaulted by nonsense:

First of all, what I said at Abnormal Returns last week is the absolute gospel:

Books > Articles Meetings > Blog Posts Conferences > Twitter

Second, each daypart should involve some sort of specific type of media consumption – just like we eat certain types of meals at certain times. What works for me:

Morning starts with my Feedly, wherein I cycle through everything published from 8pm until roughly 7am, at which time I begin curating my Hot Links post. This will often capture the print media’s stories, which hit overnight to coincide with newspaper publishing as well as the latest hilarity from Europe / Asia. I supplement Feedly first thing in the morning with Linkfest.com (aka Streeteye), which gives me the most-shared links from British Twitter (will usually feature a heavy dose of Telegraph and FT stories) as well as all the stuff that was popular with influential people overnight.

From 9am til 12noon I’m usually too busy running my practice, dealing with employees and clients, to be reading anything, which is a shame because the best financial and market bloggers usually publish their best stuff of the day in that window. Sometimes I’ll catch some interesting links off of Tweetdeck, which I keep open on my screen while multi-tasking – but it’s not easy to do this most days.

Instapaper is a great tool for me – I have a button for it on my iPad and my Chrome browser on each desktop / laptop I use. This let’s me save stuff I come upon for later.

I do a TV show four days a week from 12 til 1. I’m not reading anything here either for the most part, it’s breaking news and “what’s moving the markets today” that I’m typically involved with during this time.

Thank God that by the time I get back to my office around 1:30pm ET, the daily Abnormal Returns linkfest is usually up. I’ll scan the links and try to click on between 5 and 7 of them – hopefully read most or all of them before the afternoon’s activities kick in.

You’ll notice, at no time do I ever visit the home page of a blog or media company’s site. I rely heavily on headline scanning / curation / Twitter. You’ll also notice I don’t mention radio or TV as a part of consumption. This is deliberate. I don’t have time for the format in real-time as it requires sitting through lots of filler. Instead, I’ll try to stay attuned to appearances by specific guests and then grab the video itself. If Howard Marks or Jeff Gundlach or Cliff Asness or Warren Buffett give an interview on CNBC or Bloomberg, I want to watch it. If there’s a strategist on I care about or someone says something provocative, I figure Twitter will surface the video and circulate it. Thankfully, financial television content can be consumed a la carte and on our own time these days. We don’t have a single TV set in our offices.

Nighttime is published books for me and a stray story or two that I hadn’t gotten to from either my own Hot Links post that morning or from somewhere else like AR, or Barry’s reads list at Bloomberg View or wherever else. I’ve committed to reading more books this year than I had last year and so far I’m on pace. I aim to read a non-finance book for every finance book, for the sake of staying well-rounded and cultured.

As to my reading diet: If you want to think long-term, you can’t spend all day reading things that train your brain to twitch. When I’m not interviewing portfolio managers or other investors, I like to read the latest research in cognitive and social psychology, behavioral finance, neuroscience, financial economics, evolutionary biology and animal behavior, and financial history. (As a journalist, I get new-article alerts and press access from hundreds of academic journals. If you’re not a member of the Fourth Estate, you should closely follow the science coverage in a good newspaper like The Wall Street Journal or The New York Times.) Here, I’m looking for new findings about old truths – evidence that’s timely about aspects of human nature that are timeless.

Every investor worthy of the name must read Where Are the Customers’ Yachts? by Fred Schwed, The Money Game by ‘Adam Smith,’ Against the Gods by Peter Bernstein, the Buffett biographies by Alice Schroeder and Roger Lowenstein, A Random Walk Down Wall Streetby Burton Malkiel and The Intelligent Investor by Benjamin Graham (disclosure: I am the editor of the latest revised edition and receive a royalty on its sales, although you don’t have to read that edition). These books aren’t optional; they’re mandatory. Reading seven books is a much cheaper form of tuition than the mistakes you will make if you don’t read them.

When I’m not at work, I make a special point of reading nothing that is investment-related. I read fiction that has stood the test of time; history and historical biographies; books on science; books on art.

The “non-investing” books that every investor should read are:

Daniel Kahneman’s Thinking, Fast and Slow(disclosure: I helped Dr. Kahneman research, write and edit the book, but I don’t receive any royalties from it)

Learning how to think is a lifelong struggle, no matter how intelligent or educated you may be. Books like these will help. The chapter on time in St. Augustine’s Confessions, for instance, which I read 35 years ago, still guides me in understanding why past performance doesn’t predict future success.

Well, we’ve done it again. Augustana just launched its 154th set of graduates in your direction. Personally, it’s my 29th set of them. I think you’ll enjoy their company, if not always the quality of their prose. They’re good kids and we’ve spent an awful lot of time teaching them to ask questions more profound than “how much does it pay?” or “would you like fries with that?” We’ve tried, with some success, to explain to them that leadership flows from service, that words count, that deeds count, and that other people count.

They are, on whole, a work well begun. The other half is up to you and to them.

As for me and my colleagues, two months to recoup and then 714 more chances to make a difference.

All the noise, noise, noise, noise!

Here’s my shameful secret: I have no idea of why global stock markets at all-time highs nor when they will cease to be there. I also don’t know quite what investors are doing or thinking, much less why. Hmmm … also pretty much confused about what actions any of it implies that I should take.

I spent much of the month of May paying attention to questions like the ones implied above and my interim conclusion is that that was not a good use of my time. There are about 300 million Americans who need to make sense out of their world and about 57,000 Americans paid to work as journalists and four times that many public relations specialists who are charged with telling them what it all means. And, sadly, there’s a news hole that can never be left unfilled; that is, if you have a 30 minute news program (22.5 minutes plus commercials), you need to find 22.5 minutes worth of something to say even when you think there’s nothing to say.

And so we’re inundated with headlines like these from the May issues of The Wall Street Journal and The New York Times (noted as NYT):

Investors Abandon Riskier Assets (WSJ, May 16, C1) “Investors stepped up their retreat from riskier assets …” Except when they did the opposite four pages later:

Higher-Yielding Bank Debt Draws Interest (WSJ, May 16, C4) “Investors are scooping up riskier bonds sold by banks …”

Small Stocks Fuel a Run to Records (WSJ, May 13, C1) but then again Smaller Stocks Slammed in Selloff (WSJ, May 21, C1)

The success of “safe” strategies is encourage folks to pursue unsafe ones. Bonds Flip Scripts on Risk, Reward (WSJ, May 27, C1) “Bonds perceived as safe have produced better returns than riskier ones for the first time since 2010… in response, many investors are doubling down on riskier debt.”And so Riskier Fannie Bonds Are Devoured (WSJ, May 21, C1).

Market Loses Ground as Investors Seek Safety (NYT, May 14) “The stock market fell back from record levels on Wednesday as investors decided it was better to play it safe… ‘There’s some internal self-correction and rotation going on beneath the surface,’ said Jim Russell, a regional investment director at U.S. Bank.” But apparently that internal self-correction self-corrected within nine days because Investors Show Little Fear (WSJ, May 23, C1) “Many traders say they detect little fear in the market lately. They cite a financial outlook that is widely perceived to pose little risk of an economic or market downturn: near-record stock prices, low interest rates, steady if unspectacular U.S. growth and expansive if receding Federal Reserve support for the economy and financial markets.”

And so the fearless fearful are chucking money around:

Penny Stocks Fuel Big-Dollar Dreams (WSJ, May 23, C1) “Investors are piling into the shares of small, risky companies at the fastest clip on record, in search of investments that promise a chance of outsize returns. Investors are buying up so-called penny stocks … at a pace that far eclipses the tech boom of the 1990s.” The author notes that average trading volume is up 40% over last year which was, we’ll recall, a boom year for stocks.

Investors Return to Emerging World (WSJ, May 29, C1) “Investors are settling in for another ride in emerging markets … The speed with which investors appear to have forgotten losses of 30% in some markets has been startling.”

Searching for Yield, at Almost Any Price (NYT, May 1) “Fixed-income investors trying to increase their income essentially have two options. One is to extend maturities. The other is to reduce credit quality. There are risks to both. The prices of long-term bonds fall sharply when interest rates go up. Lower-quality bonds are more likely to default. These days, lower quality, rather than longer maturities, seems to be more popular. Money has poured into mutual funds that invest in bank loans — often low-quality ones. To a lesser extent, it has also gone into high-yield mutual funds that buy bonds rated below investment grade, known as junk bonds to those who are dubious of them.”

So, all of this risk-chasing means that it’s Time to Worry About Stock Market Bubbles (NYT, May 6) “Relative to long-term corporate earnings – and more in a minute on why that measure is important – stocks have been more expensive only three times over the past century than they are today, according to data from Robert Shiller, a Nobel laureate in economics. Those other three periods are not exactly reassuring, either: the 1920s, the late 1990s and in the prelude to the 2007 financial crisis.” … Based on history, stocks look either very expensive or somewhat expensive right now. Mr. Shiller suggests that the most likely outcome may be worse returns in coming years than the market has delivered over recent decades – but still better than the returns of any other investment class.” Great. Worst except for all the others.

Good news, though: there’s no need to worry about stock market bubbles as long as people are worrying about stock market bubbles. That courtesy of the Leuthold Group, which argues that bubbles are only dangerous once we’ve declared that there is no bubble but only a new, “permanently high plateau.”

Happily, our Republican colleagues in the House agree and seem to have decided that none of the events of 2007-08 actually occurred. Financial Crisis, Over and Already Forgotten (NYT, May 22) “Michael S. Barr, a law professor at the University of Michigan who was an assistant Treasury secretary when the financial crisis was at its worst, is working on a book titled Five Ways the Financial System Will Fail Next Time. The first of them, he says, is ‘amnesia, willful and otherwise,’ regarding the causes and consequences of the crisis. Let’s hope the others are not here yet [since a]mnesia was on full view this week.”

Wait! Wait! Josh Brown is pretty sure that they did occur, might well re-occur and probably still won’t get covered right:

Okay can we be honest for a second?

The similarities between now and the pre-crisis era are f**king sickening at this point.

There, I said it.

(After a couple paragraphs and one significant link.)

To recap – Volatility is nowhere to be found – not in currencies, in fixed income or in equities. Complacency rules the day as investors and institutions gradually add more risk, using leverage and increasingly exotic vehicles to reach for diminishing returns in an aging bull market. This as economic growth – led by housing and consumer spending – stalls out and the Fed removes stimulus that never really worked in the first place.

And once again, the media is oblivious for the most part, fixated as it is on a French economist and the valuations of text messaging startups.

You wouldn’t imagine that those of us who try to communicate for a vocation might argue that you need to read (watch and listen) less, rather than more but that is the position that several of us tend toward.

Tadas Viskanta , proprietor of the very fine Abnormal Returns blog, calls for “a news diet” in his book, Abnormal Returns: Winning Strategies from the Frontlines of the Investment Blogosphere (2012). He argues:

A media diet, as practiced by Nassim Taleb, is a conscious effort to decrease the amount of media we consume. Most of what we consume is “empty calories.” Most of it has little information value and can only serve to crowd out other more interesting and informative sources.

That’s all consistent with Barry Ritzholz’s argument that the stuff which makes great and tingly headlines – Black Swans, imminent crashes, zombie apocalypses – aren’t what hurts the average investor most. We’re hurt most, he says during a presentation at the FPA NorCal Conference in 2014, by the slow drip, drip, drip of mistakes: high expenses, impulsive trading and performance chasing. None of which is really news.

Josh Brown, who writes under the moniker The Reformed Broker at a blog of the same name, disagrees. One chapter of this new book The Clash of the Financial Pundits (2014)is entitled “The Myth of the Media Diet.” Brown argues that we have no more ability to consistently abstain from news than we have to consistently abstain from sugary treats. In his mind, the effort of suppressing the urge in the first place just leads to cheating and then a return, unreformed, to our original destructive habits: “A true media diet virtually assures an overreaction to market volatility and expert prognostication once the dieter returns to the flashing lights and headlines.” He argues that we need to better understand the financial media in order to keep intelligently informed, rather than entirely pickled in the daily brew.

And Snowball’s take on it all?

I actually teach about this stuff for a living, from News Literacy to Communication and Emerging Technologies. My best reading of the research supports the notion that we’ve become victims of continuous partial attention. There are so many ways of reaching us and we’re so often judged by the speed of our response (my students tell me that five minutes is the longest you can wait before responding to text without giving offense), that we’re continually dividing our attention between the task at hand and a steady stream of incoming chatter. (15% of us have interrupted sex to take a cellphone call while a third text while driving.) It’s pervasive enough that there are now reports in the medical literature of sleep-texting; that is, hearing an incoming text while asleep, rousing just enough to respond and then returning to sleep without later knowing that any of this had happened. We are, in short, training ourselves to be distracted, unsure and unfocused.

Fortunately, we can also retrain ourselves to become more focused. Focus requires discipline; not “browsing” or “link-hopping,” but regular, structured attention. In general, I pay no attention to “the news” except during two narrow windows each day (roughly, the morning when I have coffee and read two newspapers and during evening commutes). During those windows, I listen to NPR News which – so far as I can determine – has the most consistently thoughtful, in-depth journalism around.

But beyond that, I do try to practice paying intense and undivided attention to the stuff that’s actually important: I neither take and make calls during my son’s ballgames, I have no browser open when my students come for advice, and I seek no distraction greater than jazz when I’m reading a book.

It’s not smug self-indulgence, dear friends. It’s survival. I really want to embrace my life, not wander distractedly through it. For investors, that means making fewer, more thoughtful decisions and learning to trust that you’ve gotten it right rather than second-guessing yourself throughout the day and night.

How Good Is Your Fund Family?

Question: How many funds at Dodge & Cox beat their category average returns since inception?

Answer: All of them.

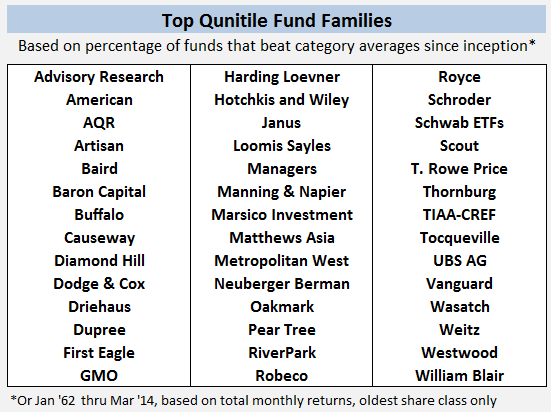

In the case of Dodge & Cox, “all” is five funds: DODBX, DODFX, DODGX, DODIX, and DODWX. Since inception, or at least as far back as January 1962, through March 2014, each has beaten its category average.

Same is true for these families: First Eagle, Causeway, Marsico, and Westwood.

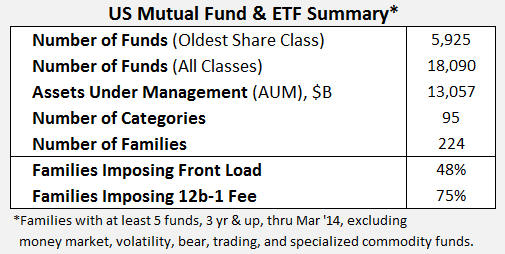

For purposes of this article, a “fund family” comprises five funds or more, oldest share class only, with each fund being three years or older.

Obviously, no single metric should be used or misused to select a fund. In this case, fund lifetimes are different. Funds can perform inconsistently across market cycles. Share class representing “oldest” can be different. Survivorship bias and category drift can distort findings. Funds can be mis-categorized or just hard to categorize, making comparisons less meaningful.

Finally, metrics based on historical performance may say nothing of future returns, which is why analysis houses (e.g., Morningstar) examine additional factors, like shareholder friendliness, experience, and strategy to identify “funds with the highest potential of success.”

In the case of Marsico, for example, its six funds have struggled recently. The family charges above average expense ratios, and it has lost some experienced fund managers and analysts. While Morningstar acknowledges strong fund performance within this family since inception, it gives Marsico a negative “Parent” rating.

Nonetheless, these disclaimers acknowledged, prudent investors should know, as part of their due diligence, how well a fund family has performed over the long haul.

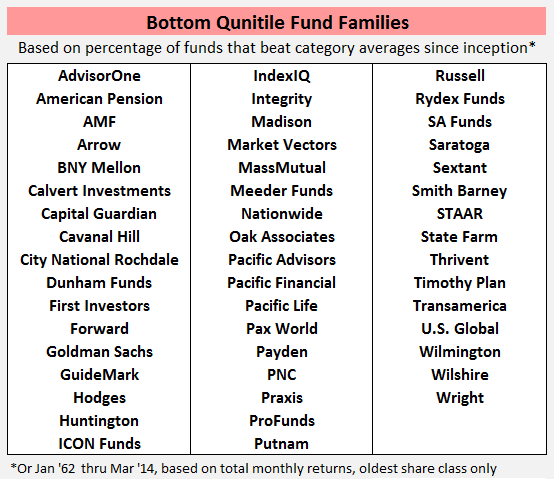

So, question: How many funds at Pacific Life beat category average returns since inception?

Applying the same criteria as above, the sad truth is: None of them.

PL funds are managed by Pacific Life Fund Advisors LLC, a wholly owned subsidiary of Pacific Life Insurance Company of Newport Beach, CA. Here from their web-site:

Got that?

Same sad truth for these families: AdvisorOne, Praxis, Integrity, Oak Associates, Arrow Funds, Pacific Financial, and STAAR.

In the case of Oak Associates, its seven funds have underperformed against their categories by 2.4% every year for almost 15 years! (They also experience maximum drawdown of -70.0% on average, or 13.1% worse than their categories.) Yet it proudly advertises recent ranking recognition by US News and selection to Charles Schwab’s OneSource. Its motto: “A Focus on Growth.”

To be clear, my colleague Professor Snowball has written often about the difficulties of beating benchmark indices for those funds that actually try. The headwinds include expense ratios, loads, transaction fees, commissions, and redemption demands. But the lifetime over- and under-performance noted above are against category averages of total returns, which already reflect these headwinds.

Overview. Before presenting performance results for all fund families, here’s is an overall summary, which will put some of the subsequent metrics in context:

It remains discouraging to see half the families still impose front load, at least for some share classes – an indefensible and ultimately shareholder unfriendly practice. Three quarters of families still charge shareholders a 12b-1 fee. All told shareholders pay fund families $12.3 billion every year for marketing. As David likes to point out, there are more funds in the US today than there are publically traded US companies. Somebody must pay to get the word out.

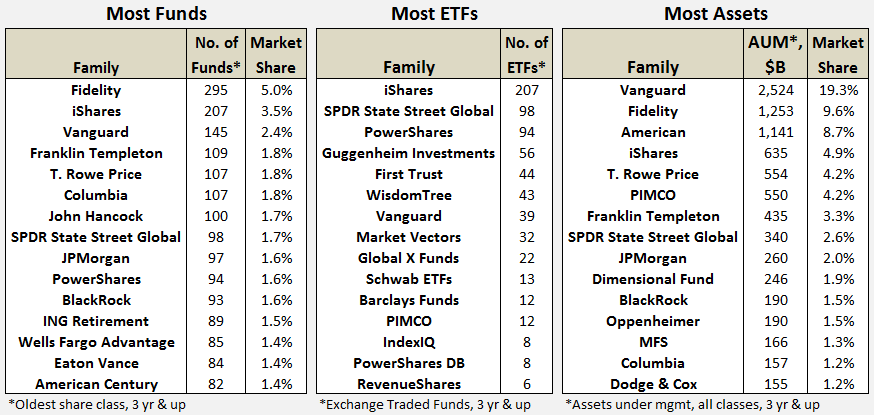

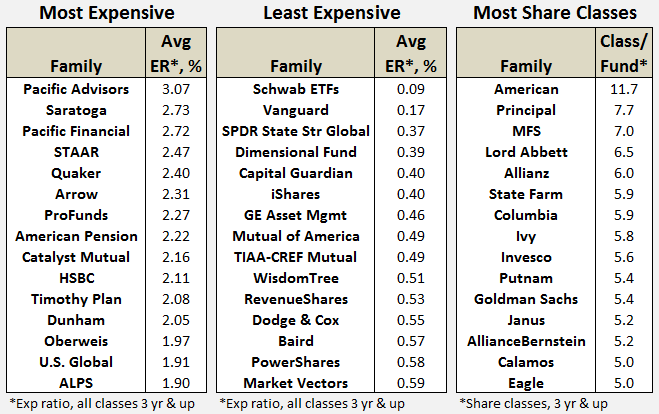

Size. Fidelity has the most number of funds. iShares has the most ETFs. But Vanguard has the largest assets under management.

Expense. In last month’s MFO commentary, Edward Studzinski asked: “It Costs How Much?”

As a group, fund families charge shareholders $83.3 billion each year for management fees and operating costs, which fall under the heading “expense ratio.” ER includes marketing fees, but excludes transaction fees, loads, and redemption fees.

It turns out that no fund family with an average ER above 1.58% ranks in the top performance quintile, as defined below, and most families with an average ER above 2.00 end up in the bottom quintile.

While share class does not get written about very often, it helps reveal inequitable treatment of shareholders for investing in the same fund. Typically, different share classes charge different ERs depending on initial investment amount, load or transaction fee, or association of some form. American has the largest number of share classes per fund with nearly five times the industry average.

Rankings. The following tables summarize top and bottom performing families, based on the percentage of their funds with total returns that beat category averages since inception:

As MFO readers would expect, comparison of top and bottom quintiles reveals the following tendencies:

Top families charge lower ER, 1.06 versus 1.45%, on average

Fewer families in top quintile impose front loads, 21 versus 55%

Fewer families in top quintile impose 12b-1 fees, 64 versus 88%

For this sample at least, the data also suggests:

Top families have longer tenured managers, if slightly, 9.6 versus 8.2 years

Top families have fewer share classes, if slightly (1.9 versus 2.3 share class ratio, after 6 sigma American is removed as an outlier; otherwise, just 2.2 versus 2.3)

The complete set of metrics, including ER, AUM, age, tenure, and rankings for each fund family, can be found in MFO Fund Family Metrics, a downloadable Google spreadsheet. (All metrics were derived from Morningstar database found in Steel Mutual Fund Expert, dated March 2014.)

A closer look at the complete fund family data also reveals the following:

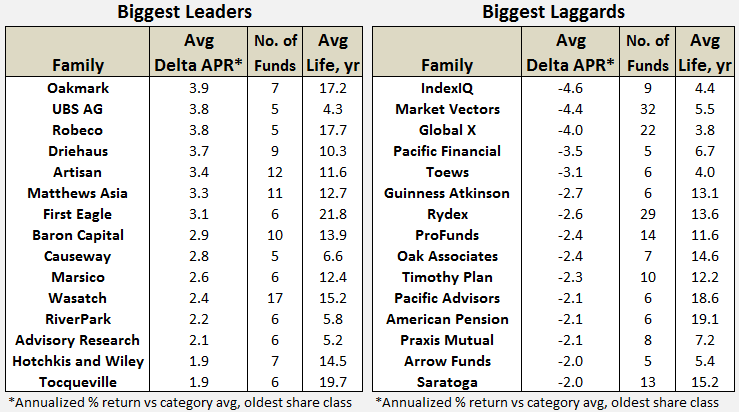

Some fund families, like Oakmark and Artisan, have beaten their category averages by 3-4% every year for more than 10 years running, which seems quite extraordinary. Whether attributed to alpha, beta, process, people, stewardship, or luck…or all the above. Quite extraordinary.

While others, frankly too many others, have done just the opposite. Honestly, it’s probably not too hard to figure out why.

On May 19, 2014, the Department of Justice nailed CS for conspiracy to commit tax fraud. At base, they allowed US citizens to evade taxes by maintaining illegal foreign accounts on their behalf. CS pled guilty to one criminal charge, which dents the otherwise universal impulse “to neither admit nor deny” wrongdoing. In consequence, they’re going to make a substantial contribution to reducing the federal budget deficit. CS certainly admits to wrong-doing, they have agreed to pay “over $1.8 billion” to the government, to ban some former officials, and to “undertake certain remedial actions.” The New York Times reports that the total settlement will end up around $2.6 billion dollars. The Economist calls it $2.8 billion.

Critics of the settlement, including Senator John McCain of Arizona, were astonished that the bank was not required to turn over the names of the tax cheats nor were “any officers, directors or key executives individually accountable for wrongdoing.” Comparable action against UBS, another Swiss bank with a presence in the US mutual fund market, in 2009 forced them to disclose the identities of 4700 account holders. The fact that CS seems intent to avoid discovering the existence of wrongdoing (the Times reports that the firm “did not retain certain documents, failed to interview potentially culpable bankers before they left the firm, and did not start an internal inquiry” for a long while after they had reason to suspect a crime), some argue that the penalties should have been more severe and more targeted at senior management.

If you want to get into the details, the Times also has a nice online archive of the legal documents in the case.

Here’s the good news part: CS reports that “The recent settlements … do not involve the Funds or Credit Suisse Asset Management, LLC, Credit Suisse Asset Management Limited or Credit Suisse Securities (USA) LLC [and] will not have any material impact on the Funds or on the ability of the CS Service Providers to perform services for the Funds.” Of course the fact that CSAM is tied to a criminal corporation would impede their ability to run US funds except for a “temporary exemptive order” from the SEC “to permit them to continue serving as investment advisers and principal underwriters for U.S.-registered investment companies, such as the Funds. Due to a provision in the law governing the operation of U.S.-registered investment companies, they would otherwise have become ineligible to perform these activities as a result of the plea in the Plea Agreement.”

If the SEC makes permanent its temporary exemptive order, then CSAM could continue to manage the funds albeit with the prospect of somewhat-heightened regulatory interest in their behavior. If the commission does not grant permanent relief, the house of cards will begin to tumble.

Which is to say, the SEC is going to play nice and grant the exemption.

One other bit of good news for CS and its shareholders: at least you’re not BNP Paribas which was hoping to get off with an $8 billion slap on the wrist but might actually be on the hook for $10 billion in connection with its assistance to tax dodgers.

Another argument for a news diet: Reuters on the end of the world

A Reuter’s story of May 28 reads, in its entirety:

BlackRock CEO says leveraged ETFs could ‘blow up’ whole industry

May 28 (Reuters) – BlackRock Inc Chief Executive Larry Fink said on Wednesday that leveraged exchange-traded funds contain structural problems that could “blow up” the whole industry one day.

Fink runs a company that oversees more than $4 trillion in client assets, including nearly $1 trillion in ETF assets.

“We’d never do one (a leveraged ETF),” Fink said at Deutsche Bank investment conference in New York. “They have a structural problem that could blow up the whole industry one day.”

Didja notice anything perhaps missing from that story? You know, places where the gripping narrative might have gotten just a bit thin?

How about: WHAT DOES “BLOW UP” EVEN MEAN? WHAT INDUSTRY EXACTLY? Or WHY?

Really, guy, you claim to be covering the end of the world – or of the investment industry or ETF industry or something – and the best you could manage was 75 words that skipped, oh, every essential element of the story?

Observer Fund Profiles:

Each month the Observer provides in-depth profiles of between two and four funds. Our “Most Intriguing New Funds” are funds launched within the past couple years that most frequently feature experienced managers leading innovative newer funds. “Stars in the Shadows” are older funds that have attracted far less attention than they deserve.

Dodge & Cox Global Bond (DODLX): Dodge & Cox, which has been helping the rich stay rich since the Great Depression, is offering you access to the world’s largest asset class, international bonds. Where their existing Income fund (DODIX) is domestic and centered on investment-grade issues, Global Bond is a converted limited partnership that can go anywhere and shows a predilection for boldness.

RiverNorth/Oaktree High Income (RNOTX): “high income” funds are often just high-yield bond funds with a handful of dividend stocks tossed in for flavor. RiverNorth and Oaktree promise a distinctive and principled take on the space: they’re allocating resources tactically between three very distinct high-income asset classes. Oaktree will pursue their specialty in senior loan and high-yield debt investing while RiverNorth continues to exploit inefficiency and volatility with their opportunistic closed-end fund strategy. They are, at base, looking for investors rational enough to profit from the irrationality of others.

Lookin’ goooood!

As you’ve noticed, the Observer’s visual style is pretty minimalist – there are no flashing lights, twirling fonts, or competing columns and there’s pretty minimal graphic embellishment. We’re shooting for something that works well across a variety of platforms (we know that a fair chunk of you are reading this on your phone or tablet while a brave handful are relying on dial-up connections).

From time to time, fund companies commission more visually appealing versions of those reprints. When they ask for formatted reprints, two things happen: we work with them on what are called “compliance edits” so that they don’t run afoul of FINRA regulations and, to a greater or lesser extent, our graphic design team (well, Barb Bradac is pretty much the whole team but she’s really good) works to make the profiles more visually appealing and readable.

Those generally reside on the host companies’ websites, but we thought it worthwhile to share some of the more recent reprints with folks this month. Each of the thumbnails opens into a full .pdf file in a separate tab.

A sample of recent reprints:

Beck, Mack & Oliver

Tributary Balanced

Evermore Global Value

Intrepid Income

Guinness Atkinson Inflation Managed Dividend

RiverPark/Gargoyle Hedged Value

And what about the other hundred profiles?

We’ve profiled about a hundred funds, all of which are accessible under the Funds tab at the top of the page. Through the kind of agency of my colleague Charles, there’s also a monthly update for every profiled fund in his MFO Dashboard, which he continues to improve. If you want an easy, big picture view, check out the Dashboard – also on the Funds page.

Elevator Talk: David Bechtel, Principal, Barrow All-Cap Core (BALAX / BALIX)

Since the number of funds we can cover in-depth is smaller than the number of funds worthy of in-depth coverage, we’ve decided to offer one or two managers each month the opportunity to make a 200 word pitch to you. That’s about the number of words a slightly manic elevator companion could share in a minute and a half. In each case, I’ve promised to offer a quick capsule of the fund and a link back to the fund’s site. Other than that, they’ve got 200 words and precisely as much of your time and attention as you’re willing to share. These aren’t endorsements; they’re opportunities to learn more.

Barrow All-Cap Core has the unusual distinction of sporting a top tier five year record despite being less than one year old. The secret is that the fund began life as a private partnership at the end of 2008. It was designed as a public equity vehicle run by private equity investors.

Their argument is that they understand both value and business prospects in ways that are fundamentally different than typical stock investors do. Combining both operating experience with a record of buying entire companies, they’re used to different metrics and different perspectives.

While you might be tempted to dismiss that as “big talk,” two factors might moderate your skepticism. First, their portfolio – typically about 200 names – really is way different from their competitors’. While Morningstar benchmarks them against the large-value group (a style box in which Barrow places just 5% of their money), the fund nearly reversed the size profile of its peers: it has about 20% in large caps, 30% in mid caps and 50% in small caps. Its peer group has about 80% in large caps. The entire portfolio is invested in six sectors, with effectively zero exposure to the four others (including financials and tech). By almost any measure (long-term earnings growth, level of corporate debt, free cash flow generation), their portfolio is substantially higher-quality than its peers. Second, the strategy’s performance – primarily as a private partnership, lately as a mutual fund – has been absolutely first tier: top 3% since inception 12/31/08 and in the top 20% in every calendar year since inception. Overall they’ve earned about 20% annually, better than both the S&P 500 and its large-value peers.

BALAX is managed by Nicholas Chermayeff, formerly of Morgan Stanley’s Principal Investment Group, and Robert F. Greenhill, who co-founded Barrow Street Advisors LLC, the fund’s advisor, after a stint at Goldman Sachs’ Whitehall Funds. Both are Harvard graduates (unlike some of us). The Elevator Talk itself, though, was provided by Yale graduate David Bechtel, a Principal of Barrow Street Advisors LLC, the fund’s advisor, who serves on its Investment Committee, and advises on the firm’s business development activities. He is a Founder and Managing Member of Outpost Capital Management LLC which structures and manages investments in the natural resources and financial services sectors. Mr. Bechtel offered just a bit more than 200 words to explain Barrow’s distinctiveness:

We are, first and foremost, private equity investors. Since Barrow Street was founded in 1997, we have invested and managed hundreds of millions in private market opportunities. The public equity strategy (US stocks only) used in Barrow All-Cap was funded by our own capital in 2008.

We launched this strategy and the fund to meet what we viewed as a market need. We take a private equity approach to security selection. We are not a “value” manager – selecting stocks based on low p/e, etc. – nor a pure “quality” manager – buying blue chips at any price. We look for very high quality companies whose shares are temporarily trading at a discount.

We look at value and quality the way a control investor in a business would. We emphasize cash flow, sales growth per unit of capital, operating margins, and we like companies that reinvest in their businesses. That gives us a very good feeling that not only is the management team interested in growing their business, but also that the business itself is good at generating cash.

On the valuation side, we’re looking for firms that are “momentarily” trading well-below intrinsic value. The general idea is to look at total enterprise value – equity market cap plus debt and preferred stock minus cash on the books – which controls for variations on capital structures, leverage, etc.

We’re trying to differentiate by combining our private equity approach to quality and value into one strategy at the security selection level. And, we are just as dedicated to portfolio diversification to help our investors better weather market volatility. It’s a portfolio without compromises. We think that’s very unusual in the mutual fund universe.

The fund has both institutional and retail share classes. The retail class (BALAX) has a $2500 minimum initial investment. Expenses are 1.41% with about $22 million in assets. The institutional share class (BALIX) is $250,000 and 1.16%. Here’s the fund’s homepage. The content there is modest but useful.

Funds in Registration

Funds currently in registration with the SEC will generally be available for purchase some time in July, 2014. Our dauntless research associate David Welsch tracked down 12 new no-load funds in registration this month. While there are no immediately tantalizing registrants, there are two flexible bond funds being launched by well-respected small fund families (Weitz Core Plus Income and William Blair Bond Fund) plus the conversion of a pretty successful private options-hedged equity strategy (V2 Hedged Equity Fund, though I would prefer that we not name our investments after the Nazi “Vengeance Weapon 2”).

The manager change story-of-the-month comes from S&P Capital IQ. While the report is not publicly available, its conclusion is widely reported: “Of 6,185 U.S. equity mutual funds tracked by Rosenbluth’s firm, more than a thousand of them, or 16.3%, have experienced a manager change since February 2011.” Oddly, the journalists reporting on the story including Brendan Conaway at Barron’s and the Mutual Fund Wire staff, don’t seem to ask the fundamental question: how often does it matter? They do point to do instances cited by Rosenbluth (Janus Contrarian and Fidelity Growth & Income) where the manager change was worth noting, but don’t ask how typical those cases are.

A far more common pattern, however, is that what’s called a “fund manager change” is actually a partial shuffle of an existing management team. For example, our May “manager changes” feature highlighted 52 manager changes but 36 of those (70% of the total) were partial changes. Example would be New Covenant Growth Fund (NCGFX) where one of the 17 members of the management team departed, Fidelity Series Advisor Growth Opportunities Fund (FAOFX) where there’s a long-term succession strategy or a bunch of the Huntington funds where no one left but a new co-manager was added to the collection.

Speaking of manager changes, Chip this month tracked down 57 sets of them.

Updates: the Justin Frankel/Josh Brown slapfest over liquid alts

Josh Brown, the above-named “reformed broker,” ran a piece in mid-May entitled Brokers, Liquid Alts and the Fund that Never Goes Up. He discusses the fate of Andrew Lo and ASG Diversifying Strategies Fund (DSFAX):

Dr. Andrew Lo vehicle called ASG Diversifying Strategies Fund. The idea was that Dr. Lo, perhaps one of the most brilliant quantitative scientists and academicians in finance (MIT, Harvard, all kinds of awards, PhDs out the ass, etc), would be incorporating a variety of approaches to manage the fund using all asset classes, derivatives and trading methodologies that he and his team saw fit to apply.

What actually did happen was this: Andy Lo, maybe one of the smartest men in the history of finance, managed to invent a product that literally cannot make money in any environment. It’s an extraordinarily rare accomplishment; I don’t think you could go out and invent something that always loses money if you were actually attempting to.

Brown’s argument is less with liquid alts as an arena for investing, and more with the brokers who continue to push investors into a clearly failed strategy.

Justin Frankel, probably the only RiverPark manager that we haven’t spoken with and co-manager of RiverPark Structural Alpha Fund (RSAFX), quickly rushed to the barricades to defend Alt-land from the barbarian horde (and, in doing so, responded to an argument that Brown wasn’t actually making). He published his defense on, of all things, his Tumblr page:

The Wall Street machine has a long history of favoring institutions over individuals, and the ultra-high net worth over the mass affluent. After all, finance is a service industry, and it is those larger clients that pay the lion’s share of fees.

Liquid Alternatives are simply hedge fund strategies wrapped in a mutual fund format … From a practical standpoint, investors should view these strategies as a way to diversify either bond or stock holdings in order to provide non-correlated returns to their investment portfolios, cushion portfolios against downside risks, and improve risk-adjusted returns.

Individual investors have become more sophisticated consumers of financial products. Liquid Alternatives are not just a democratization of the alternative investing landscape. They represent an evolution in how investors can gain access to strategies that they could never invest in before.

Frankel’s argument is redolent of Morty Schaja’s stance, that RiverPark is bringing hedge fund strategies to the “mass affluent” though with a $1000 minimum, they’re available to the mass mass, too.

Both pieces, despite their possibly excessive fraternity, are worth reading.

Briefly Noted . . .

Manning and Napier is adding options to the funds in their Pro-Blend series. Effective on July 14, 2014, the funds will gain the option of writing (which is to say, say selling) options on securities and pursuing a managed futures (a sort of asset-class momentum) strategy. And since the Pro-Blend funds are used in Manning & Napier’s target-date retirement funds, the strategy changes ripple into them, too.

This month, most especially, I’m drawing on the great good work of The Shadow in tracking down the changes below. “Go raibh mile maith agaibh as bhur gcunamh” big guy! Thanks, too, to the folks on the discussion board for their encouragement during the disruptions caused by my house move this month.

SMALL WINS FOR INVESTORS

Donald P. Carson, formerly the president of an Atlanta-based investment holding company and now a principal at Ansley Securities, joined the Board of The Cook & Bynum Fund (COBYX) in April and has already made an investment in the fund in the range of $100,001 – $500,000. Two things are quite clear from the research: (1) having directors – as distinct from managers – invested in a fund improves its risk-return profile and (2) it’s relatively rare to see substantial director investment in a fund. The managers are deeply invested in the fund and it’s great that their directors are, too.

The Osterweis funds (Osterweis, Strategic Income, Strategic Investment and Institutional Equity) will all, effective June 30 2014 drop their 30-day, 2.0% redemption fees. I’m always ambivalent about eliminating such fees, since they discourage folks from trading in and out of funds, but most folks cheer the flexibility so we’re willing to declare it “a small win.”

Effective May 16, 2014, the minimum initial investment on the institutional class of the RiverPark funds (Large Growth, RiverPark/Wedgewood Fund, Short Term High Yield, Long/Short Opportunity, RiverPark/Gargoyle Hedged Value, Structural Alpha Fund and Strategic Income) were all reduced from $1,000,000 to $100,000. Of greater significance to many of us, the expense ratios were reduced for Short Term High Yield (from 1.25% to 1.17% on RPHYX and from 1.00% to 0.91% on RPHIX) and RiverPark/Wedgewood (from 1.25% to 1.05% on RPCFX and from 1.00% to 0.88% on RWGIX).

CLOSINGS (and related inconveniences)

Effective on July 8, 2014, Franklin Biotechnology Discovery Fund (FBDIX) will close to new investors. It’s a fund for thrill seekers – it invests in very, very growth-y midcap biotech firms which are (ready for this?) really volatile. The fund’s returns have averaged about 12% over the past decade – 115 bps better than its peers – but the cost has been high: a beta of 1.77 and a standard deviation nearly 50% about the Specialty-Health group norm. That hasn’t been enough to determine $1.3 billion in investment from flowing in.

Morningstar’s been having real problems with their website this month. During the last week of the month, some fund profiles were completely unavailable while, in other cases, clicking on the link to one fund would take you to the profile of another. I assume something similar is going on here, since the MPT data for this biotech stock fund benchmarks it against “BofAML Convertible Bonds All Qualities.”

Update:

One of the Corporate Communication folks at Morningstar reached out in response to my comment on their site stability which itself was triggered mostly by the vigorous thread on the point.

Ms. Spelhaug writes: “Hope you’re well. I saw your column mentioning issues you’ve experienced with the Quote pages on Morningstar.com. I wanted to let you know that we’re aware that there have been some issues and have been in the process of retiring the system that’s causing the problems.”

Effective as of May 30, 2014, the investor class of Samson STRONG Nations Currency Fund (SCRFX) closed its “Investor” class to new investors. On that same day, those shares were re-designated as Institutional Class shares. Given the fund’s parlous performance (down about 8% since inception compared to a peer group that’s down about 0.25%), the closure might be prelude to …. uhhh, further action.

T. Rowe Price Capital Appreciation (PRWCX) will close to new investors on June 30, 2014. Traditionally famous for holding convertible securities, the fund’s fixed-income exposure is almost entirely bonds now with a tiny sliver of convertibles. That reflects the manager’s judgment that converts are way overpriced. The equity part of the portfolio targets blue chips, though the orientation has slowly but surely shifted toward growthier stocks over the years.

The fund is bloated at over $20 billion in assets but it’s sure hard to criticize. It’s posted peer-beating returns in 11 of the past 12 years, including all five years since crossing the $10 billion in AUM threshold. It’s particularly impressive that the fund has outperformed Prospector Capital Appreciation (PCAFX), which is run by Richard Howard, PRWCX’s long-time manager, over the past seven years. While I’m generally reluctant to recommend large funds, much less large funds that are about to close, this one really does warrant a bit of attention on your part.

All classes of the Wells Fargo Advantage Discovery Fund (WFDAX) are closed to new investors. The $3.2 billion fund has posted pretty consistently above average returns, but also consistently above average risks.

OLD WINE, NEW BOTTLES

Effective July 1, 2014, the AllianzGI Structured Alpha Fund (AZIAX) will change its name to the AllianzGI Structured Return Fund. Its investment objective, principal investment strategies, management fee and operating expenses change as well. The plan is to write exchange-traded call options or FLEX call options (i.e. listed options that are traded on an exchange, but with customized strike prices and expiration dates) to generate income and some downside protection. The choice strikes me as technical rather than fundamental, since the portfolio is already comprised of 280 puts and calls. The most significant change is a vast decrease in the fund’s expense ratio, from 1.90% for “A” shares down to 1.15%.

Crow Point Hedged Global Equity Income Fund (CGHAX) has been rechristened Crow Point Defined Risk Global Equity Income Fund. The Fund’s investment objective, policies and strategies remain unchanged.

Hansberger International Growth (HIGGX/HITGX) is in the process of becoming one of the Madison (formerly Mosaic) Funds. I seem to have misread the SEC filing last month and reported that they’re becoming part of the Madison Fund (singular) rather than Madison Funds (plural). The management team is responsible for about $4 billion in mostly institutional assets. They’re located in, and will remain in, Toronto. This will be Madison’s second international fund, beside Madison NorthRoad International (NRIEX) whose managers finish their third solid year at the helm on June 30th.

Effective June 4 2014, the Sustainable Opportunities (SOPNX) fund gets renamed the Even Keel Multi-Asset Managed Risk Fund. The Fund’s investment objective, policies and strategies remain unchanged. Given the fund’s modest success over its first two years, I suppose there are investors who might have preferred keeping the name and shifting the strategy.

The Munder Funds are in the process of becoming Victory funds. Munder Capital Management, Munder’s advisor, got bought by Victory Capital Management, so the transition is sensible and inevitable. Victory will create a series of “shell” funds which are “substantially similar, if not identical” to existing Munder funds, then merge the Munder funds into them. This is all pending shareholder approval.

Touchstone Core Bond Fund has been renamed Touchstone Active Bond Fund (TOBAX). The numbers on the fund are a bit hard to decipher – by some measures, lots of alpha, by others

Effective on or about July 1, 2014, Transamerica Diversified Equity (TADAX) will be renamed Transamerica US Growth and the principal investment strategy will be tweaked to require 80% U.S. holdings. Roughly speaking, TADAX trailed 90% of its peers during manager Paul Marrkand’s first calendar year. The next year it trailed 80%, then 70% and so far in 2014, 60%. Based on that performance, I’d put it on your buy list for 2019.

OFF TO THE DUSTBIN OF HISTORY

On May 29, 2014 (happy birthday to me, happy birthday to me …), the tiny and turbulent long/short AllianzGI Redwood Fund (ARRAX) was liquidated and dissolved.

The Giralda Fund (GDAIX) liquidates its “I” shares on June 27, 2014 but promises that you can swap them for “I” shares of Giralda Risk-Managed Growth Fund (GRGIX) if you’d really like.

Harbor Target Retirement 2010 Fund (HARFX) has changed its asset allocation over time in accordance with its glide path and its allocation is now substantially similar to that of Harbor Target Retirement Income Fund, and so 2010 is merging into Retirement Income on Halloween. Happily, the merger will not trigger a tax bill.

In mid-May, 2014, Huntington suspended sales of the “A” and institutional shares of its Fixed Income Securities, Intermediate Government Income, Mortgage Securities, Ohio Tax-Free, and Short/Intermediate Fixed Income Securities funds.

On May 16, 2014, the Board of Trustees of Oppenheimer Currency Opportunities Fund (OCOAX) approved a plan to liquidate the Fund on or about August 1, 2014. Since inception, the fund offered its investors the opportunity to turn $100 into $98.50 which a fair number of them inexplicably accepted.

At the recommendation of LSV Asset Management, the LSV Conservative Core Equity Fund (LSVPX) will cease operations and liquidate on or about June 13, 2014. Morningstar has it rated as a four-star fund and its returns have been in the top decile of its large-value peer group over the past five years, which doesn’t usually presage elimination. As the discussion board’s senior member Ted puts it, “With only $15 Million in AUM, and a minimum investment of $100,000 hard to get off the ground in spite of decent performance.”

Turner All Cap Growth Fund (TBTBX) is slated to merge into Turner Midcap Growth Fund (TMGFX) some time in the fall of 2014. Since I’ve never seen the appeal of Turner’s consistently high-volatility funds, I mostly judge nod and mumble about tweedle-dum and …

Wilmington’s small, expensive, risky, underperforming Large-Cap Growth Fund (VLCPX) and regrettably similar Large-Cap Value Fund (VEINX) have each been closed to new investors and are both being liquidated around June 20th.

In Closing . . .

The Morningstar Investment Conference will be one of the highlights of June for us. A number of folks responded to our offer to meet and chat while we’re there, and we’re certainly amenable to the idea of seeing a lot more folks while we’re there.

I don’t tweet (despite Daisy Maxey’s heartfelt injunction to “build my personal brand”) but I do post a series of reports to our discussion board after each day at the conference. If you’re curious and can’t be in Chicago, please to feel free to look in on the board.

Finally, thanks to all those who continue to support the Observer – with their ideas and patience, as much as with their contributions and purchases. It’s been a head-spinning time and I’m grateful to all of you as we work through it.

Just a quick reminder that we’re going to clean our email list. We’ve got two targets, addresses that make absolutely no sense and folks who haven’t opened one of our emails in a year or more.

The fund tries to provide total return, rather than just income. The strategy is to divide the portfolio between two distinctive strategies. Oaktree Capital Management pursues a “barbell-shaped” strategy consisting of senior bank loans and high-yield debt. RiverNorth Capital Management pursues an opportunistic closed-end fund (CEF) strategy in which they buy income-producing CEFs when those funds are (1) in an attractive sector and (2) are selling at what the manager’s research estimates to be an unsustainable discount to NAV. In theory, the entire portfolio might be allocated to any one of the three strategies; in practice, RiverNorth anticipates a “neutral position” in which 25 – 33% of the portfolio is invested in CEFs.

Adviser

RiverNorth Capital Management. RiverNorth is a Chicago-based firm, founded in 2000 with a distinctive focus on closed-end fund arbitrage. They have since expanded their competence into other “under-followed, niche markets where the potential to exploit inefficiencies is greatest.” RiverNorth advises the five RiverNorth funds: Core (RNCOX, closed), Managed Volatility (RNBWX), Equity Opportunity (RNEOX), RiverNorth/DoubleLine Strategic Income (RNDLX) and this one. They manage about $1.9 billion through limited partnerships, mutual funds and employee benefit plans.

Manager

Patrick Galley and Stephen O’Neill of RiverNorth plus Desmund Shirazi, Sheldon M. Stone and Shannon Ward of Oaktree. Mr. Galley is RiverNorth’s founder, president and chief investment officer; Mr. O’Neill is the chief trader, a remarkably important position in a firm that makes arbitrage gains from trading on CEF discounts. Mr. Shirazi is one of Oaktree’s senior loan portfolio managers, former head of high-yield research and long-ago manager of TCW High Yield Bond. Ms. Ward, who joined this management team just a year ago, was a vice president for high-yield investments at AIG back when they were still identified with The Force. The RiverNorth portion of the team manages about $2 billion in assets. The Oaktree folks between them manage about $200 million in mutual fund assets and $25 billion in private accounts and funds.

Strategy capacity and closure

In the range of $1 billion, a number that the principals agree is pretty squishy. The major capacity limiter is the fund’s CEF strategy. When investors are complacent, CEF discounts shrink which leaves RiverNorth with few opportunities to add arbitrage gains. The managers believe, though, that two factors will help keep the strategy limit high. First, “fear is here to stay,” so investor irrationality will help create lots of mispricing. Second, on March 18 2014, RiverNorth received 12(d)1 exemptive relief from the SEC. That exemption allows the firm to own more than 3% of a CEF’s outstanding shares, which then expands the amount they might profitably invest.

Management’s stake in the fund

The RiverNorth Statement of Additional Information is slightly screwed-up on this point. It lists Mr. Galley as having either $0 (page 33) or “more than $100,000” (page 38). The former is incorrect and the latter doesn’t comply with the standard reporting requirement where the management stake is expressed in bands ($100,000-500,000, $500,000 – $1 million, over $1 million). Mr. O’Neill has between $10,000 and $50,000 in the fund. The Oaktree managers and, if the SAI is correct, the fund’s directors have no investment in the fund.

Opening date

December 28, 2012

Minimum investment

$5,000, reduced to $1,000 for IRAs.

Expense ratio

1.44% for “I” class shares and 1.69% for “R” class shares on assets of $54.9 million, as of July 2023.

Comments

In good times, markets are reasonably rational. In bad times, they’re bat-poop crazy. The folks are RiverNorth and Oaktree understand you need income regardless of the market’s mood, and so they’ve attempted to create a portfolio which operates well in each. We’ll talk about the strategies and then the managers.

What are these people up to?

The managers will invest in a variable mix of senior loans, high yield bonds and closed-end funds.

High yield bonds are a reasonably well understood asset class. Firms with shaky credit have to pay up to get access to capital. Structurally they’re like other bonds (that is, they suffer in rising rate environments) but much of their attraction arises from the relatively high returns an investor can earn on them. As investors become more optimistic about the economy, the premium they demand from lower-credit firms rises; as their view darkens, the amount of premium they demand rises. Over the past decade, high yield bonds have earned 8.4% annually versus 7.4% for large cap stocks and 6.5% for investment–grade corporate bonds. Sadly, investors crazed for yield have flooded into high-yield bonds, driving up their prices and driving their yield down to 5.4% in late May.

Senior loans represent a $500 billion asset class, which is about the size of the high-yield bond market. They represent loans made to the same sorts of companies which issue high-yield bonds. While the individual loans are private, collections of loans can be bundled together and sold to investors (a process called “securitizing the loans”). These loans have two particularly attractive structural features: they have built-in protection against loss of principal because they’re “senior” in the firm’s capital structure, which means that there’s collateral behind them and their owners would receive preferential treatment in the case of a bankruptcy. Second, they have built-in protection against loss of interest because they’re floating rate loans; as interest rates rise, so does the amount paid to the loan’s owner. These loans have posted positive returns in 15 of the past 16 years (2008 excepted).

In general, these loans yield a lot more than conventional investment grade bonds and operate with a near-zero correlation to the broad bond market.

Higher income. Protection against loss of capital. Protection against rising rates. High diversification value. Got it?

Closed-end funds share characteristics of traditional mutual funds and of other exchange-traded securities, like stocks and ETFs. Like mutual funds, they represent pools of professionally managed securities. The amount that one share of a mutual fund is worth is determined solely by the value of the securities in its portfolio. Like stocks and ETFs, CEFs trade on exchanges throughout the day. The amount one share of a CEF is worth is not the value of the securities in its portfolio; it’s whatever someone is willing to pay you for the share at any particular moment in time. Your CEF share might be backed by $100 in stocks but if you need to sell it today and the most anyone will offer is $70, then that share is worth $70. The first value ($100) is called the CEF’s net asset value (NAV) price, the second ($70) is called its market price. Individual CEFs have trading histories that show consistent patterns of discounts (or premiums). A particular fund might always have a market price that’s 3% below its NAV price. If that fund is sudden available at a 30% discount, an investor might buy a share that’s backed by $100 in securities for $70 and sell it for $97 when panic abates. Even if the market declined 10% in the interim, the investor could still sell a share purchased as $70 for $87 (a 10% NAV decline and a 3% discount) when rationality returns. As a result, you might pocket gains both from picking a good investment and from arbitrage as the irrational discount narrows; that arbitrage gain is independent of the general direction of the market.

RiverNorth/Oaktree High Income combines these three high-income strategies: an interest-rate insensitive loan strategy and a rate-sensitive high-yield one plus an opportunistic market-independent CEF arbitrage strategy.

Who are these guys, and why should we trust them?

Oaktree Capital Management was founded in April 1995 by former TCW professionals. They specialize in specialized credit investing: high yield bonds, convertible securities, distressed debt, real estate and control investments (that is, buying entire firms). They manage about $80 billion for clients on five continents. Among their clients are 100 of the 300 largest global pension plans, 75 of the 100 largest U.S. pension plans, 300 endowments and foundations, 11 sovereign wealth funds and 38 state retirement plans in the United States. Oaktree is widely recognized as an extraordinarily high-quality firm with a high-quality investment discipline.

To be clear: these are not the sorts of clients who tolerate carelessness, unwarranted risk taking or inconsistent performance.

RiverNorth Capital Management pursues strategies in what they consider to be niche markets where inefficiencies abound. They’re the country’s pre-eminent practitioner of closed-end fund arbitrage. That’s most visible in the (closed) RiverNorth Core Opportunity Fund (RNCOX), which has $700 million in assets and five-year returns in the top 13% of all moderate allocation funds. A $10,000 investment made in RNCOX at inception would be worth $19,000 by May 2014 while its average competitor would have returned $14,200.

Their plan is to grow your money steadily and carefully.

Patrick Galley describes this as “a risk-managed, high-yield portfolio” that’s been “constructed to maximize risk-adjusted returns over time, rather than shooting for pure short-term returns.” He argues that this is, in his mind, the central characteristic of a good institutional portfolio: it relies on time and discipline to steadily compound returns, rather than luck and boldness which might cause eye-catching short term returns. As a result, their intention is “wealth preservation: hit plenty of singles and doubles, rely on steady compounding, don’t screw up and get comfortable with the fact that you’re not going to look like a hero in any one year.”

Part of “not screwing up” requires recognizing and responding to the fact that the fund is investing in risky sectors. The managers have the tactical freedom to change the allocation between the three sleeves, depending on evolving market conditions. In the fourth quarter of 2013, for example, the managers observed wide discounts in CEFs and had healthy new capital flows, so they quickly increased CEF allocation to over 40% from a 25-33% neutral position. They’re now harvesting gains, and the CEF allocation is back under 30%.

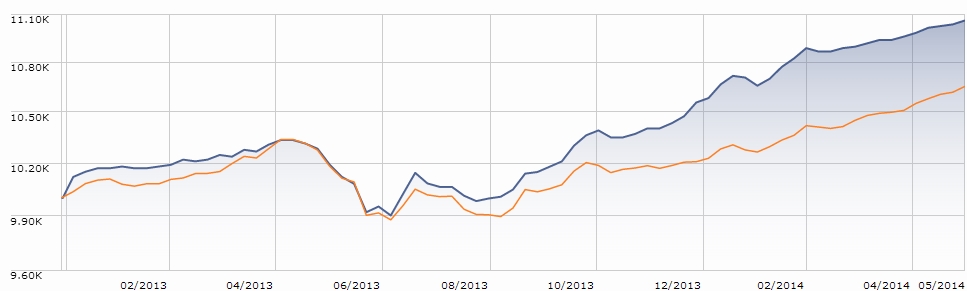

So far, they’ve quietly done exactly what they planned. The fund is yielding 4.6% over the past twelve months. It has outperformed its multi-sector bond benchmark every quarter so far. Below you can see the comparison of RNOTX (in blue) and its average peer (in orange) from inception through late May 2014.

Bottom Line

RNOTX is trying to be the most sensible take possible on investing in promising, risky assets. It combines two sets of extremely distinguished investors who understand the demands of conservative shareholders with an ongoing commitment to use opportunism in the service of careful compounding. While this is not a low-risk fund, it is both risk-managed and well worth the attention of folks who might otherwise lock themselves into a single set of high-yield assets.

Fund website

RiverNorth/Oaktree High Income. Interested in becoming a better investor while you’re browsing the web? You really owe it to yourself to read some of Howard Marks’ memos to Oaktree’s investors. They’re about as good as Buffett and Munger, but far less known by folks in the mutual fund world.

DODLX is seeking a high rate of total return consistent with long-term preservation of capital. They’ll invest in both government and corporate securities, including those of firms domiciled in emerging markets. They begin with a set of macro-level judgments about the global economy, currency fluctuation and political conditions in various regions. The security selection process seems wide-ranging. They’re able to hedge currency, interest rate and other risks.

Adviser

Dodge & Cox was founded in 1930, by Van Duyn Dodge and E. Morris Cox. The firm, headquartered in San Francisco, launched its first mutual fund (now called Dodge & Cox Balanced) in 1931 then added four additional funds (Stock, Income, International and Global Stock) over the next 85 years. Dodge & Cox manages around $200 billion, of which $160 billion are in their mutual funds. The remainder is in 800+ separate accounts. Their funds are all low-cost, low-turnover, value-conscious and team-managed.

Managers

Dana Emery, Diana Strandberg, Thomas Dugan, James Dignan, Adam Rubinson, and Lucinda Johns. They are, collectively, the Global Bond Investment Policy Committee. The fact that the manager bios aren’t mentioned, and then briefly, until page 56 of the prospectus but the SAI lists the brief bio of every investment professional at the firm (down to the assistant treasurer) tells you something about the Dodge culture. In any case, the members have been with D&C for 12 – 31 years and have a combined 116 years with the firm.

Strategy capacity and closure

Unknown, but the firm is prone to large funds. They’re also willing to close those funds and seem to have managed well the balance between performance and assets.

Management’s stake in the fund

Unknown since the fund opened after the reporting data in the SAI. That said, almost every director has a substantial personal investment in almost every fund, and every director (except a recent appointee, who has under $50,000 but has been onboard for just one year) has over $100,000 invested with the firm. Likewise every member of the Investment Committee invests heavily in every D&C; most managers have more than $1 million in each fund. The smallest reported holding is still over $100,000.

Opening date

December 5, 2012 if you count the predecessor fund, a private partnership, or May 1, 2014 if you date it from conversion to a mutual fund.

Minimum investment

$2,500 initial minimum investment, reduced to $1,000 for IRAs.

Expense ratio

0.45% on assets of $1.9 Billion, as of July 2023.

Comments

Many people assume that the funds managed by venerable “white shoe” firms are automatically timid. They are not. They are frequently value-conscious, risk-conscious, tax-conscious and expense-conscious. They are frequently very fine. But they are not necessarily timid. Welcome to Dodge & Cox, a firm founded during the Great Depression to help the rich remain rich. They are, by all measures, an exemplary institution. Their funds are all run by low-profile teams of long-tenured professionals and they are inclined to avoid contact with the media. Their decision-making is legitimately collective and their performance is consistently admirable. Here’s the argument for owning what Dodge & Cox sells:

Name

Ticker

Inception

M* Ranking

M* Analyst Rating

M* Expenses

Balanced

DODBX

1931

Four star

Gold

Low

Global Stock

DODWX

2008

Four star

Gold

Low

International Stock

DODFX

2001

Four star

Gold

Low

Income

DODIX

1989

Four star

Gold

Low

Stock

DODGX

1965

Four star

Gold

Low

Here’s the argument against it:

Assets, in billions

Peer rank in 2008

M* risk

Great Owl or not

MFO Risk Group

Balanced

DODBX

15

Bottom 11%

High

No

Above average

Global Stock

DODWX

5

n/a

Above average

No

Average

International Stock

DODFX

59

Bottom 18%

Above Average to High

No

High

Income

DODIX

26

Top third

Average

No

High

Stock

DODGX

56

Bottom 9%

Above Average

No

High

The sum of the argument is this: D&C is independent. They have perspectives not shared by the vast majority of their competitors. When they encounter what they believe to be a fundamentally good idea, they move decisively on it. Sometimes their decisive moves are premature, and considerable dislocation can result. Dodge & Cox Global Fund started as a private partnership and documents filed with the SEC suggests that the fund had a single shareholder. As a result, the portfolio could be quite finely tuned to the risk tolerance of its investors. The fund’s current portfolio contains 25.4% emerging markets bonds. It has 14% of its money in Latin American bonds (the average global bond fund has 1%) and 5% in African bonds (versus 1%). 59% of the bond is rated by Moody’s as Baa (lower medium-grade bonds) or lower. Those imply a different risk-return profile than you will find in the average global bond fund. Why worry about a global bond fund at all? Four reasons come to mind:

International bonds now represent the world’s largest asset class: about 32% of the total value of the global stock and bond market, up from 19% of the global market in 2000.

The average American investor has very limited exposure to non-U.S. bonds. Vanguard’s analysis (linked below) concludes “ U.S. investors generally have little, if any, exposure to foreign bonds in their portfolios.”

The average American investor with non-U.S. bond exposure is likely exposed to the wrong bonds. Both index funds and timid managers replicate the mistakes embodied in their indexes: they weight their portfolios by the amount of debt issuance rather than by the quality of issuer. What does that mean? It means that most bond indexes (hence most index and closet-index funds) give the largest weighting to whoever issues the greatest volume of debt, rather than to the issuers who are most capable of repaying that debt promptly and in full.

Adding “the right bonds” to your portfolio will fundamentally improve your portfolio’s risk/return profile. A 2014 Vanguard study on the effects of increasing international bond exposure reaches two conclusions: (1) adding unhedged international bonds increases volatility without offsetting increase in returns because it represents a simple currency bet but (2) adding currency-hedged international bond exposure decreases volatility in almost all portfolios. They report:

It is interesting that, once the currency risk is removed through hedging, the least-volatile portfolio is 42% U.S. stocks, 18% international stocks, and 40% international bonds. Further, with bond currency risk negated, the inclusion of international bonds has relatively little effect on the allocation decision regarding international stocks. In other words, a 30% allocation to international stocks within the equity portion of the portfolio (18% divided by 60%) remains optimal for reducing volatility over the period analyzed, regardless of the level of international bond allocation.

This makes it easier for investors to assess the impact of adding international bonds to a portfolio. In addition, we find that hedged international bonds historically have offered consistent risk-reduction benefits: Portfolio volatility decreases with each incremental allocation to international bonds.

The greatest positive effect they found was from the addition of emerging markets bonds.

Bottom Line

The odds favor the following statement: DODLX will be a very solid long-term core holding. The managers’ independence from the market, but dependence on D&C’s group culture, will occasionally blow up. If you check your portfolio only once every three-to-five years, you’ll be very satisfied with D&C’s stewardship of your money.

Because bond fund managers, traditionally, had made relatively modest impacts of their funds’ absolute returns, Manager Changes typically highlights changes in equity and hybrid funds.

Ticker

Fund

Out with the old

In with the new

Dt

CLACX

AdvisorOne Select Appreciation Fund

Matthew Santini

Grant Engelbart

5/14

CLSHX

AdvisorOne Shelter Fund

Stephen Donahoe

Scott Kubie, who previously managed the fund from 2009 to 2011, returns.

5/14

AAPAX

American Beacon Retirement Income and Appreciation Fund

Jeff Scudieri is out

The rest of the team remains on the fund.

5/14

AIVOX

American Century International Opportunities Fund

Indraneel Das is out

Mark Kopinski and Trevor Gurwich remain

5/14

MMCIX

BNY Mellon Small/Mid Cap Multi-Strategy Fund, formerly the BNY Mellon Small/Mid Cap Fund

As part of the name and strategy change, John Truschel is out.

The team of David Daglio, James Boyd, Stephanie Brandaleone, Joseph Corrado, Dale Dutile, Bernard Schoenfeld, Todd Wakefield, Edward Walter, and Robert Zeuthen, is in

5/14

CLTAX

Catalyst/Lyons Tactical Allocation

Michael Schoonover

Louis Stevens resumes the lead.

5/14

CASAX

Columbia Pacific/Asia Fund

No one, but . . .

Christine Seng joins Daisuki Nomoto and Jasmine Huang

5/14

DMVAX

Dreyfus Select Managers Small Cap Value Fund

No one, but . . .

Channing Capital Management has been added as a subadvisor, with Wendell Mackey joining the management team.

5/14

KTRAX

DWS Global Income Builder Fund

Benjamin Price is out

The rest of the team remains on the fund.

5/14

SEMGX

DWS Investments

Juergen Foerster and Johannes Prix are out

Sean Taylor and Andrew Beal take over

5/14

EAFVX

Eaton Vance Focused Value Opportunities Fund

Matthew Beaudry and Stephen Kaszynski are out immediately. In addition, Michael Mach will retire from Eaton Vance on June 30.

John Crowley will remain as lead portfolio manager. He will be joined by Edward Perkin on June 30.

5/14

EHSTX

Eaton Vance Large-Cap Value Fund

Matthew Beaudry and Stephen Kaszynski are out immediately. In addition, lead portfolio manager Michael Mach will retire from Eaton Vance on June 30.

John Crowley will remain as lead portfolio manager. He will be joined by Edward Perkin, who will become lead portfolio manager, on June 30.

5/14

EATVX

Eaton Vance Tax-Managed Value Fund

Matthew Beaudry and Stephen Kaszynski are out immediately. In addition, lead portfolio manager Michael Mach will retire from Eaton Vance on June 30.

John Crowley will remain as lead portfolio manager. He will be joined by Edward Perkin, who will become lead portfolio manager, on June 30.

5/14

FDASX

Fidelity Advisor Global Strategies Fund

Andrew Dierdorf and Jurrien Timmer are gone

Christopher Sharpe and Ruben Calderon are the new managers.

5/14

FDYSX

Fidelity Global Strategies Fund

Andrew Dierdorf and Jurrien Timmer are gone from a fund that the Observer has been deeply skeptical of

Christopher Sharpe and Ruben Calderon are the new managers, which doesn’t really abate the doubts.

5/14

FENRX

Forward Endurance Long/Short Fund

David Readerman will no longer be involved in the day-to-day management of the fund

Jim O’Donnell will carry on as the sole portfolio manager

5/14

FFSCX

Forward Small Cap Equity Fund

David Readerman will no longer be involved in the day-to-day management of the fund

Jim O’Donnell will carry on as the sole portfolio manager

5/14

HKMNX

HAGIN Keystone Market Neutral Fund

Nathan Lee will no longer serve as a portfolio manager

The remainder of the team, Robert Morris, Patrick Morris, and Kyle Cox, carries on.

5/14

HIACX

Hartford Capital Appreciation HLS Fund

Paul Marrkand leaves the team

Philip Ruedi joins the team

5/14

HLEAX

Hartford Global Research Fund

Cheryl Duckworth and Mark Mandel are no longer portfolio managers

Ian Link, W. Michael Reckmeyer, and John Ryan are in.

5/14

HSCSX

Homestead Small Company Stock Fund

No one right now, but Peter Morris and Stuart Teach will be retiring sometime next year.